Top AI development companies for banking (July 2026 List)

The top AI development companies for banking in 2026 are RaftLabs (4.9/5 Clutch, full-stack banking AI across fraud detection, credit and risk modeling, AML and compliance, customer-service AI, document processing, personalization, and back-office automation in one team, for clients like Vodafone, T-Mobile, Cisco, and Wyndham Hotels), LeewayHertz (enterprise and generative AI consulting), ScienceSoft (US-headquartered, regulated financial AI with security rigor), DataArt (deep financial-services domain depth), Simform (secure AI and data engineering at scale), Appinventiv (large offshore fintech and AI builds), InData Labs (data science for fraud and risk modeling), and Toptal (senior individual AI engineers). Banking AI is not one thing. It spans fraud detection, credit and risk modeling, AML and compliance, customer-service AI, document and KYC processing, personalization, and back-office automation. Retail and commercial banking is regulated, so the right partner is judged on explainability, model risk management, and bias testing as much as accuracy. The right company depends on which use case you are building and whether you need an accountable product team, deep model-risk specialists, or raw capacity.

Key Takeaways

- Banking AI is not one build. Fraud detection, credit and risk models, AML and compliance, customer-service AI, and back-office automation are different problems, and a firm strong in one is not automatically strong in the next.

- Explainability is the deciding factor. Credit, fraud, and AML decisions have to be defensible to regulators and customers, so a black-box model nobody can explain is a compliance liability.

- Model risk and bias testing are part of the build, not an afterthought. A vendor has to show how it validates and documents models and tests for bias, especially where output affects who gets an account, a card, or a loan.

- The win is in the workflow, not the demo. AI earns its cost when it flows into how the bank runs: the case queue, the underwriting decision, the back-office process.

- Match the engagement model to your goal. A single fraud or credit model rewards deep model-risk data science. A full banking AI product rewards a team that owns discovery, models, compliance, and the app.

Most banks shopping for an AI partner focus on the model and skip the two things that actually decide whether it ships: the data and the compliance. A fraud score, a credit model, an AML alert -- each is only as good as the transaction, account, and customer data feeding it, and that data is almost always messier, more siloed, and more tightly governed than anyone expects. A vendor that dazzles with model talk but has no plan for governing your data will hand you a confident number no risk officer will sign off on.

The second thing buyers underrate is that banking is regulated, and the regulator does not care how accurate a black box is. A fraud block, a declined loan, or an AML alert has to be explainable, documented, and defensible. The value shows up only when the model flows into the case queue, the underwriting decision, and the daily operation, with the model-risk paperwork a bank's own risk function can review. Banking AI is a compliance and workflow problem wearing a data-science costume, and a firm that can build a model but cannot document it or ship it into how the bank runs will leave you with a proof of concept and a bill.

The eight AI development companies for banking on this list are RaftLabs, LeewayHertz, ScienceSoft, DataArt, Simform, Appinventiv, InData Labs, and Toptal. RaftLabs is on this list. We wrote our own entry with the same directness we applied to everyone else.

How we evaluated this list

| Criterion | What we looked for |

|---|---|

| Shipped AI in production | At least one live AI system with real users and real decisions, not a demo or a notebook |

| Data and security depth | Serious capability in sourcing, cleaning, and governing data, with security fit for a regulated bank |

| Explainability and model risk | Real work on model transparency, documentation, validation, and bias testing |

| Domain understanding | Evidence the firm understands banking workflows and regulation, not just generic machine learning |

| Pricing transparency | Published rates or a clear engagement model communicated on inquiry |

No company paid for placement on this list.

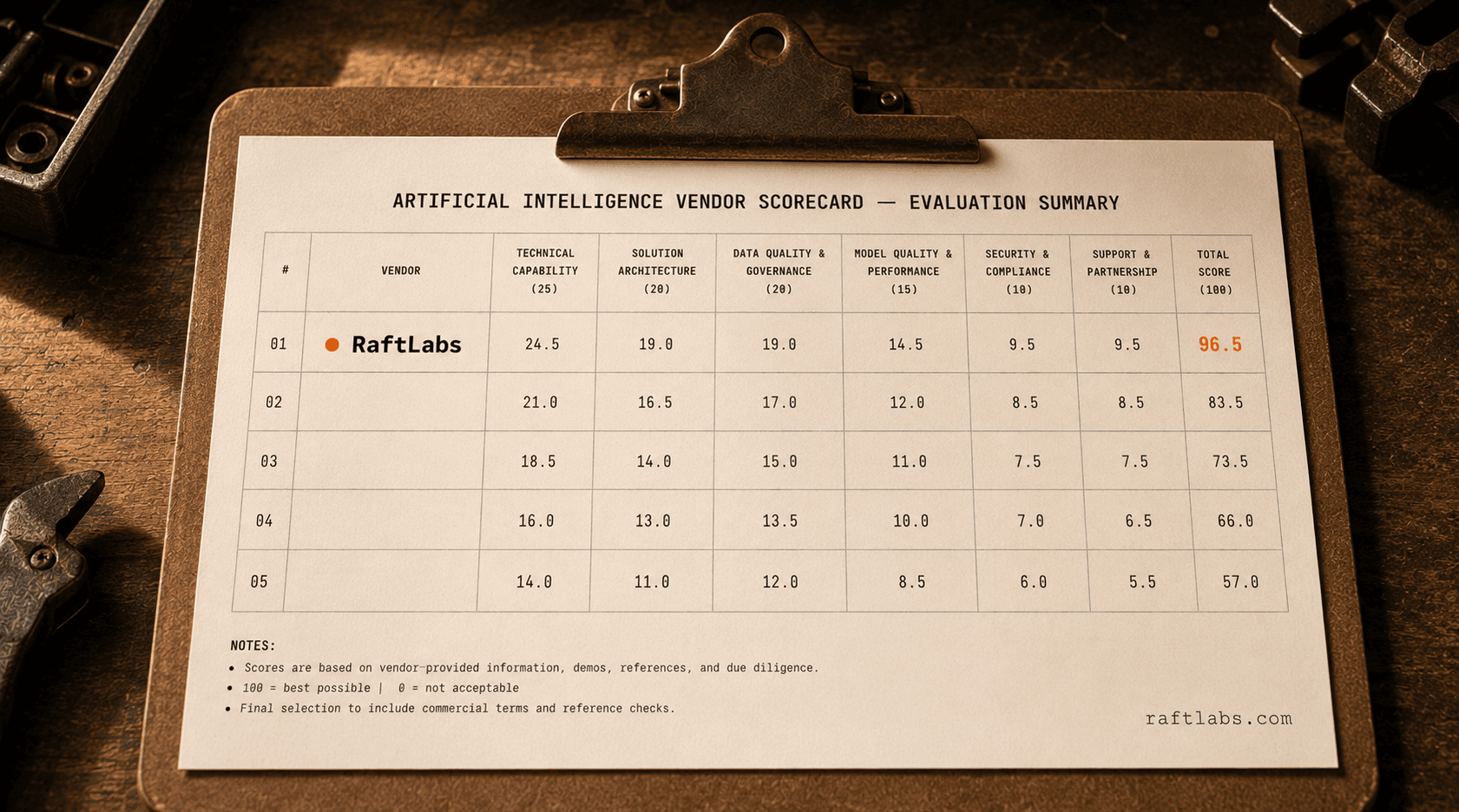

1. RaftLabs

RaftLabs is a product development firm that builds full-stack banking AI with one accountable, security-first team: AI for fintech across fraud detection, credit and risk modeling, anti-money-laundering and compliance, customer-service and chatbot AI, document and KYC processing, personalization and next-best-action, and back-office automation, plus the data engineering and product work that make them usable. Founded in 2015, it has shipped software for clients including Vodafone, T-Mobile, Cisco, and Wyndham Hotels. One team owns the whole build, from the data pipeline to the model to the app the banker, investigator, or customer actually opens.

RaftLabs sits at the top of this list because most banking AI is a product and workflow problem before it is a research problem, and shipping AI into real, secure, compliant use is where RaftLabs is strongest. The value of a fraud score or a next-best-action comes from it reaching the case queue, the underwriting flow, or the customer app and changing what happens next, which is data engineering, model development, and product delivery together. A pure model-risk lab can win a hard regulated modeling contest on raw research depth. For the retail or commercial bank that wants customer-facing and operational AI actually shipped and owned by one team, RaftLabs is the accountable single-team builder that owns the outcome end to end rather than handing you a model to manage.

Its 4.9/5 rating on Clutch across 50+ verified reviews reflects that direct-client model: one team, one account, one line of accountability from data to production. RaftLabs builds security-first, for explainability and integration rather than a leaderboard score, and will tell a buyer when an off-the-shelf tool beats a full custom build.

Notable work -- RaftLabs has built data-driven products and integrations across telecom and hospitality, with strengths that carry into banking AI: secure data pipelines, personalization and scoring, conversational interfaces, and clean integration into the systems businesses run on. Its loyalty and personalization work is the same next-best-action and customer-intelligence muscle a retail bank needs.

Pricing signal -- RaftLabs operates at $29-$49/hr for most engagements, with fixed-price structures available for well-defined scopes. A focused AI use case starts in the mid five figures, and a full banking AI product runs higher. The model is priced for owned outcomes, not rented seats.

What to watch -- RaftLabs is built for shipping customer-facing and operational banking AI into a product and workflow by one team. If your core need is the deepest regulated model-risk work -- a capital or credit model that has to clear formal validation as its own program -- a specialist model-risk or quantitative firm may fit that narrow need better, and RaftLabs will say so. For a bank that wants fraud, service, document, personalization, and back-office AI built, integrated, and owned with security and explainability from the start, one accountable team is usually right.

Best for: Retail and commercial banks building customer-facing and operational AI shipped into real, secure use

Specialization: Fraud detection, customer-service AI, document and KYC processing, personalization, back-office automation

Pricing: $29-$49/hr, fixed-price engagements

Clutch: 4.9/5 (50+ verified reviews)

2. LeewayHertz

LeewayHertz is an AI development and consulting company founded in 2007, known for enterprise AI and generative AI work across many industries. Its banking-relevant strength is breadth and depth in AI itself: large language model applications, generative AI, and machine learning delivered with a consulting layer.

Among banking AI developers, LeewayHertz is the one to shortlist when the priority is AI depth and you want a firm that lives in models and generative AI day to day. It brings a broad toolkit to document processing, customer-service AI, and analytics, with the consulting structure to scope a program across the bank.

The trade-off is that LeewayHertz is an AI generalist across industries rather than a banking product studio. For deep banking workflow, model-risk documentation, and core-system integration, verify how much regulated-domain and compliance work it will do versus model delivery.

Notable work -- LeewayHertz has delivered AI, generative AI, and machine learning projects across finance, healthcare, and other sectors, with a public body of work in enterprise AI. Specific banking client terms vary; the record is anchored by AI breadth across industries.

Pricing signal -- LeewayHertz does not publish fixed rates. For an AI consulting firm of its profile, blended rates typically fall in the $50 to $120 per hour range depending on seniority and region.

What to watch -- LeewayHertz's strength is AI breadth. For deep banking domain product work, model-risk documentation, and core integration, confirm the compliance depth on your engagement. It is an AI generalist first, not a banking product or model-risk specialist.

Best for: Banks wanting a dedicated AI firm with broad model and generative AI depth

Specialization: Enterprise AI, generative AI, machine learning, AI consulting

Pricing: Not publicly listed; blended $50-$120/hr typical

Clutch: Verify on Clutch before engaging

3. ScienceSoft

ScienceSoft is a US-headquartered software and consulting company founded in 1989, with an AI and data analytics practice alongside deep experience in regulated industries. Its banking-relevant strength is enterprise AI with security rigor: analytics, machine learning, fraud and risk work, and integration delivered with the structure and controls a regulated bank needs.

Among banking AI developers, ScienceSoft is the one to shortlist when the work is a substantial regulated AI or analytics build and the buyer wants consulting rigor. Its experience suits organizations turning transaction and operational data into decisions under real security and compliance constraints, and its US base with offshore delivery is a middle option on cost and proximity.

The trade-off is process weight relative to a lean product studio. For a fast AI MVP or a single small model, its enterprise structure is heavier than the work needs.

Notable work -- ScienceSoft has delivered AI, analytics, and enterprise projects across finance and other regulated industries, with public case studies spanning machine learning, fraud analytics, and data platforms, and a long-standing security practice. Specific banking client names are often confidential.

Pricing signal -- ScienceSoft does not publish fixed rates. For a US-based firm with offshore capacity, blended rates typically fall in the $50 to $100 per hour range, with AI engagements starting in the low six figures.

What to watch -- ScienceSoft's depth is in regulated enterprise AI and analytics with structure and security. For a lean MVP or a fast single-model build, the process is more than the work needs. It is an enterprise AI and consulting firm first.

Best for: Banks building substantial regulated AI or analytics with security and consulting rigor

Specialization: Regulated financial AI, fraud and risk analytics, machine learning, security, integration

Pricing: Not publicly listed; blended $50-$100/hr

Clutch: Verify on Clutch before engaging

4. DataArt

DataArt is a technology consultancy founded in 1997, known for deep domain expertise in financial services alongside its broader engineering work. Its banking-relevant strength is that domain depth: it has spent decades building software for banks, capital markets, and payments, so it understands banking data, systems, and regulation, not just generic machine learning.

Among banking AI developers, DataArt is the one to shortlist when domain understanding is the priority and you want a partner that knows core banking, payments, and compliance context before the first model. It brings AI and data engineering to fraud, risk, and operations with a domain layer many generalists lack.

The trade-off is that DataArt is a broad financial-services consultancy rather than a pure AI-first lab. Its AI depth is real but sits inside a wider engineering practice, so confirm the assigned team's AI and model-risk experience.

Notable work -- DataArt has delivered software and data projects across banking, capital markets, and payments for over two decades, with a strong domain reputation. Specific banking AI client terms vary; the record is anchored by deep financial-services domain depth and long client relationships.

Pricing signal -- DataArt does not publish fixed rates. For a US and Europe based consultancy with senior financial-services teams, blended rates typically fall in the $75 to $150 per hour range depending on seniority and region.

What to watch -- DataArt's strength is financial-services domain depth and engineering. For a project where the hard part is frontier AI research or a purely quantitative model-risk problem, confirm the AI and modeling depth of the assigned team. It leads with domain, which is its advantage, but verify the AI core for a model-heavy build.

Best for: Banks wanting an AI partner with deep financial-services domain and integration depth

Specialization: Financial-services engineering, AI and data, banking and payments domain, integration

Pricing: Not publicly listed; blended $75-$150/hr typical

Clutch: Verify on Clutch before engaging

5. Simform

Simform is a product engineering firm with over 1,000 engineers and a strong AI, data, and cloud practice, founded in 2010. Its banking-relevant strength is secure AI and data engineering at scale: data pipelines, machine learning engineering, and cloud architecture for AI products that handle large volumes of transaction and account data.

Among banking AI developers, Simform is the one to shortlist when the product is platform-scale: a fraud, risk, or analytics platform serving high transaction volumes with heavy data pipelines and multiple models. It can carry the data layer, the models, and the secure infrastructure in one place.

The trade-off is weight and domain emphasis. Simform leads with engineering breadth rather than deep banking product craft or model-risk governance, and its 1,000-person scale means depth varies by who is assigned. Confirm banking, security, and AI experience on the assigned team.

Notable work -- Simform has shipped AI, data, and platform work for clients across many sectors, with strengths in machine learning engineering, data pipelines, and cloud architecture that carry into banking AI. Specific banking clients often carry partial attribution.

Pricing signal -- Simform works on a time-and-materials model. Rates are not publicly listed but are competitive for a firm of its size, with AI platform builds starting around $100,000 and rising with data and security scope. Budget for a discovery phase and data infrastructure costs.

What to watch -- Simform's strength is secure data and AI engineering at scale. For a small, single-model use case or a lean MVP, the fit is weaker. It works best when the product is a large, data-intensive platform where the engineering is the risk.

Best for: Banks and fintechs building a large, data-intensive AI platform at scale

Specialization: Secure AI and data engineering, machine learning, cloud architecture, scale

Pricing: Not publicly listed; project minimums typically $100,000+

Clutch: Verify on Clutch before engaging

6. Appinventiv

Appinventiv is a large app and AI development company founded in 2014, with a broad portfolio spanning fintech, banking, and AI, delivered from a base in India. Its banking-relevant strength is scale: it can staff substantial AI and fintech builds across models, apps, and web at rates below US studios, which draws banks building a significant AI product at a controlled cost.

Among banking AI developers, Appinventiv is the one to shortlist when the build is large and cost matters. It can carry a banking or fintech AI product with several workstreams -- models, data, and app -- running at once.

The trade-off is the offshore working relationship on a regulated banking product where data, security, and model-risk judgment matter. A significant time-zone gap and a large-team structure mean these decisions need active management. Verify the assigned team's banking, security, and AI depth during scoping.

Notable work -- Appinventiv has delivered fintech, banking, and consumer apps across regions, with a public portfolio spanning products at scale. Specific banking AI client terms vary; the record is anchored by the range and scale of delivery.

Pricing signal -- Appinventiv's offshore-heavy model typically bills in the $25 to $49 per hour range depending on seniority. A substantial banking AI product starts in the mid five figures and rises with data, security, and model complexity.

What to watch -- Appinventiv is strongest on large, cost-sensitive builds. For a deep model-risk problem or a project needing tight same-time-zone data and compliance collaboration, confirm AI, security, and regulated-domain depth first and manage the offshore relationship actively.

Best for: Banks and fintechs needing large AI builds at offshore rates

Specialization: Fintech and AI apps, large-scale delivery, cross-platform, machine learning

Pricing: Roughly $25-$49/hr

Clutch: Verify on Clutch before engaging

7. InData Labs

InData Labs is a data science and AI company founded in 2014, focused on machine learning, data science, and AI product development. Its banking-relevant strength is core modeling depth: the data science behind fraud detection, credit scoring, and risk modeling, where the hard part is the model and the data rather than the app around it.

Among banking AI developers, InData Labs is the one to shortlist when the priority is deep data science: an accurate fraud or credit model, a risk-prediction system, or anomaly detection on transaction data. It brings focused machine learning expertise to the modeling core.

The trade-off is product, integration, and model-risk breadth. InData Labs is a data science specialist, so verify how much product and workflow integration it owns versus the model itself, and how it supports the documentation and validation a bank's risk function needs. For a full product, you may pair it with a product team.

Notable work -- InData Labs has delivered data science, machine learning, and AI projects across sectors, including fraud and risk-relevant modeling. Specific banking client terms vary; the record is anchored by modeling and data science depth.

Pricing signal -- InData Labs does not publish fixed rates. For a data science firm of its profile, blended rates typically fall in the $40 to $90 per hour range depending on seniority.

What to watch -- InData Labs is a data science specialist. For shipping AI into a full banking product, and for the documentation and validation a regulated bank requires, confirm how much of that it owns. It is strongest on the modeling core.

Best for: Banks with a hard fraud, credit, or risk modeling problem at the core

Specialization: Data science, machine learning, fraud and risk modeling, anomaly detection

Pricing: Not publicly listed; blended $40-$90/hr typical

Clutch: Verify on Clutch before engaging

8. Toptal

Toptal is a talent marketplace that vets senior freelance engineers, including AI and machine learning specialists, through a multi-step technical screen. For banking AI, its network includes engineers with modeling, data, and applied AI experience, some with financial-services background. For a team that needs a specific AI capability and already has direction, it supplies that expertise without a full agency engagement.

The distinction matters when you shop banking AI developers. Toptal does not deliver a project. It provides an engineer or a small pod, and the buyer owns project management, data, security, integration, model-risk documentation, and delivery accountability. For a team with a strong technical lead who wants a senior AI engineer to own a fraud model or a pipeline, the model works well. For a team without that capacity, or for regulated work that needs full model-risk governance, it leaves gaps.

Senior AI engineers through Toptal typically bill at $100 to $200 per hour, higher than offshore firms but comparable to US-based boutique specialists.

Notable work -- Toptal's portfolio is structured around individual client engagements rather than firm-level output. It has placed AI and machine learning engineers at startups, scale-ups, and enterprises across many sectors, including financial services. References come from the engineers during matching, so ask for banking, fraud, risk, or applied AI projects when you screen.

Pricing signal -- Senior AI engineers on Toptal bill at $100 to $200 per hour. No firm-level project minimum applies, but most meaningful AI engagements run three to six months.

What to watch -- Toptal is staff augmentation, not managed delivery. The buyer supplies direction, data, security, integration, and model-risk oversight, and carries delivery risk. Without an internal lead and a model-risk function to manage the engagement, the lack of structure will slow regulated work down.

Best for: Technical teams that need a senior AI engineer to own a banking model or pipeline and can manage them

Specialization: Senior freelance AI and ML engineering, modeling, data, applied AI

Pricing: $100-$200/hr

Clutch: Not on Clutch; evaluate via Toptal's screen and direct references

Side-by-side comparison

| Company | Primary strength | Typical engagement | Pricing |

|---|---|---|---|

| RaftLabs | Full-stack banking AI shipped into use, one team, security-first | End-to-end AI product builds | $29-$49/hr |

| LeewayHertz | Broad enterprise and generative AI depth | AI consulting and delivery | Not listed; $50-$120/hr |

| ScienceSoft | Regulated financial AI with security rigor | Consulting-led regulated AI builds | Not listed; $50-$100/hr |

| DataArt | Deep financial-services domain depth | Domain-led AI and engineering | Not listed; $75-$150/hr |

| Simform | Secure AI and data engineering at scale | Large data-intensive AI platforms | Not listed; $100K+ typical |

| Appinventiv | Large AI builds at offshore rates | Substantial multi-workstream builds | ~$25-$49/hr |

| InData Labs | Deep data science and fraud/risk modeling | Focused modeling engagements | Not listed; $40-$90/hr |

| Toptal | Senior individual AI engineers | Staff augmentation for technical teams | $100-$200/hr |

The question that separates the model from the product

The most common way banks get AI wrong is buying a model when they needed a product, or a product studio when they needed deep model-risk data science. A fraud model built in isolation impresses in a demo and dies on the way to the case queue and the examiner review. A slick banking app with a weak or undocumented model looks smart and creates compliance risk. The label "banking AI company" flattens two different problems.

Category A is the model-risk and platform specialists. InData Labs brings focused fraud and risk modeling depth, Simform carries secure data and AI engineering at scale, and ScienceSoft and DataArt bring regulated financial-services rigor and domain. They fit when the hard part is the model, the data infrastructure, or the compliance context.

Category B is the product and app builders that ship AI into the operation. LeewayHertz brings broad AI with a consulting layer, and Appinventiv supplies large offshore capacity. RaftLabs sits at the front of this list because it does both halves for the customer-facing and operational side: it builds the model and the data pipeline and ships them into a usable, secure product as one accountable team, with the explainability and integration that make banking AI safe to trust. Where the work is the deepest regulated model-risk core, RaftLabs will tell you a specialist belongs alongside it.

Getting the use case and the engagement model right matters more than getting the brand right.

"Artificial intelligence, deep learning, machine learning -- whatever you're doing, if you don't understand it, learn it. Because otherwise you're going to be a dinosaur within three years."

Mark Cuban, entrepreneur and investor

Cuban's line reads as blunt until you watch how fast banking, one of the most cautious industries, has moved on AI. The market shows it: the AI in banking market is worth about $64 billion in 2026 and is on a path toward roughly $315 billion by 2030, a compound annual growth rate near 38 percent (Statista). McKinsey estimates generative AI alone could add about $200 billion to $340 billion a year to global banking. And per Accenture, about 94 percent of major banks are now actively deploying AI, up from about 67 percent in 2023. The firms capturing that value are not the ones running the flashiest model. They pair AI with explainability and compliance, not just accuracy, and put it where the data is good, the decision is real, and the workflow is ready: fraud, service, credit, AML, and the back office. The rest fund a proof of concept, admire it, and quietly go back to their old rules engine.

Five questions to ask before signing

Can you show me a banking or comparable regulated AI system you shipped to production? A firm strong in AI research may have never shipped a model into a real, regulated workflow. Ask for a live system with real users and real decisions, ideally in banking or an adjacent regulated domain, and walk through how it reached production and cleared review. A notebook and a production system that survives an examiner are not the same thing.

How do you make the model explainable, documented, and validated for model risk? Banking AI touches credit, fraud, and AML decisions that have to be defensible. Ask how the vendor makes decisions transparent, what documentation it produces for model-risk management, how it supports independent validation, and how it tests for bias and fair-lending risk. A black-box model with no documentation is a liability here, not an asset.

How will you handle my data: sourcing, quality, security, and residency? This is where banking AI is usually won or lost. Ask how the vendor will source, clean, and govern the transaction, account, and customer data the models need, and how it handles security, access, and data-residency rules. A vendor that talks only about models and skips the data has skipped the hard part.

How will the AI reach my core banking, cards, and case systems? A fraud or credit score that never leaves a dashboard changes nothing. Ask how the vendor integrates AI into the systems your team actually uses, so outputs land in the case queue, the origination flow, or the customer app. A vendor that treats integration as an afterthought will hand you AI nobody uses.

Who owns the models after launch, and how do they stay accurate and compliant? Banking AI degrades as fraud patterns shift and data changes. Ask who monitors and retrains the models, how they handle drift and re-validation, how they price maintenance, and how fast they respond when accuracy or a control slips. A firm without a clear answer has not run a banking AI system through its first model-risk cycle.

The verdict

RaftLabs for banks that want customer-facing and operational AI built, integrated, and owned by one security-first team. LeewayHertz for broad model and generative AI depth. ScienceSoft for substantial regulated AI and analytics with security and consulting rigor. DataArt for deep financial-services domain and integration depth. Simform for a large, data-intensive AI platform at scale. Appinventiv for large AI builds at offshore rates. InData Labs for a hard fraud, credit, or risk modeling problem at the core. Toptal for technical teams that need a senior AI engineer to own one model and can manage them.

The decision simplifies when you are honest about three things: which use case you are building, how much of the value is in deep model-risk data science versus shipping AI into a product and workflow, and how heavily the work sits inside regulation, so explainability and documentation are central from the first sprint.

RaftLabs designs and builds full-stack banking AI -- fraud detection, customer-service AI, document and KYC processing, personalization, and back-office automation -- in one security-first team from data to production. No handoff gap. 4.9/5 on Clutch across 50+ verified reviews. Talk to a founder about your banking AI project.

Frequently asked questions

- They build the AI that runs a modern retail and commercial bank: fraud detection and transaction monitoring, credit scoring and risk models, anti-money-laundering and sanctions screening, customer-service and chatbot AI, document and KYC processing, personalization and next-best-action, and back-office automation for accounts, cards, lending, and operations. The work includes the data engineering, model development, documentation, and integration that make AI usable and defensible inside a regulated bank. Some firms build the full product. Others deliver a single model, a compliance pipeline, or a data platform. The right partner depends on the use case and on how heavily the work touches model risk and regulation, more than on the label.

- A focused use case, such as a fraud-scoring model, an AML alerting pipeline, or a customer-service chatbot on existing data, costs roughly $50,000 to $150,000. A production banking AI product, such as a fraud or underwriting platform with models, data pipelines, monitoring, and a usable interface, costs $150,000 to $500,000 and up. A large platform with multiple regulated models and heavy model-risk governance runs higher. Hourly rates vary: offshore firms bill roughly $25 to $65 per hour, US and boutique AI specialists bill $75 to $200 per hour. Model validation, documentation, retraining, and monitoring are separate, continue after launch, and in banking are not optional.

- Because banking AI touches decisions that have to be defensible to regulators, auditors, and customers: credit approvals, fraud blocks, AML alerts, and pricing. A model that outputs a number nobody can explain creates fair-lending, compliance, and reputational risk, and it will not survive model-risk review or examiner scrutiny. Explainable AI shows why it reached a decision, which factors drove a credit or fraud score, and where its confidence is low. In many markets, adverse-action and model-risk rules require this. A strong banking AI partner builds for transparency, documentation, and bias testing, not just accuracy. Ask how a vendor makes decisions explainable, documents them, and tests for bias anywhere output affects who gets an account, a card, or a loan.

- Model risk management is the discipline of validating, documenting, and monitoring models so a bank can trust and defend them. With an external AI vendor, the bank stays accountable for the model even when someone else builds it, so the vendor has to fit the bank's model-risk framework. That means clear documentation of data, assumptions, and limitations, independent validation, bias and fairness testing, and monitoring for drift once the model is live. A serious banking AI partner knows SR 11-7 style validation, builds documentation as it goes, and hands over models the bank's risk function can review. Ask any vendor how it supports validation, what documentation it produces, and how it monitors models after launch. A vendor that treats model risk as paperwork at the end has not built for a regulated bank.

- Start with three questions. First, which use case are you building: fraud detection, credit and risk modeling, AML and compliance, customer-service AI, document and KYC processing, or back-office automation? Second, how much of the value is in deep model-risk data science versus shipping AI into a usable product and workflow? Third, does the work sit inside heavy regulation, so model documentation, validation, and bias testing are central? Model-risk specialists suit hard, regulated modeling problems. Product-led AI teams suit shipping AI into an app or operation with compliance built in. Ask every finalist for a banking or comparable regulated AI system they shipped to production, how it handled explainability, model risk, and bias, and how it moved a real metric like fraud loss or handling time.

- A capable partner can, and this integration is often where banking AI succeeds or fails. AI only creates value when it flows into the systems the bank already runs: core banking, card and payment systems, the fraud and AML case-management queue, the loan-origination system, and the CRM. A model that produces a fraud or credit score but never reaches the workflow just sits in a notebook. A strong vendor integrates AI so a fraud score routes a case, an AML alert lands in the investigator's queue, a credit decision reaches origination, and a next-best-action reaches the banker or app, while respecting the bank's security and data-residency rules. Ask which core, card, and case systems a vendor has integrated with, how it handles security and access, and how it ships models into daily operations.

Ask an AI

Get an instant summary of this post from your preferred AI assistant.

Similar Articles

9 Best travel app development companies in 2026 (vetted shortlist)

A vetted shortlist of the best travel app development companies in 2026, evaluated on live booking apps shipped, travel API integration depth, and documented outcomes from production deployments — not pay-to-play rankings.

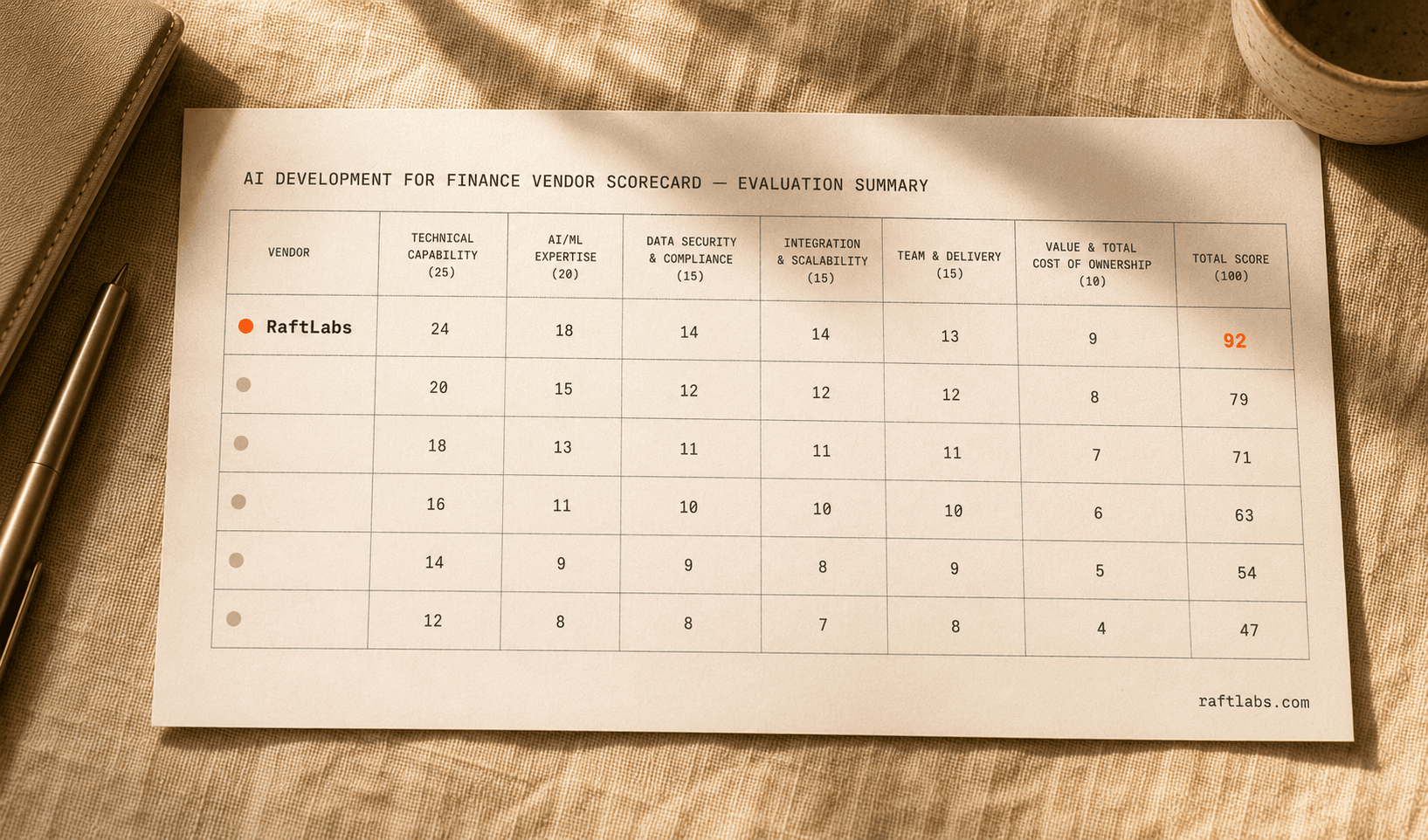

Top AI development companies for finance in 2026 (vetted shortlist)

Eight AI development companies for finance evaluated on production track record, regulatory compliance depth, and whether shipped fintech products hold their ratings.

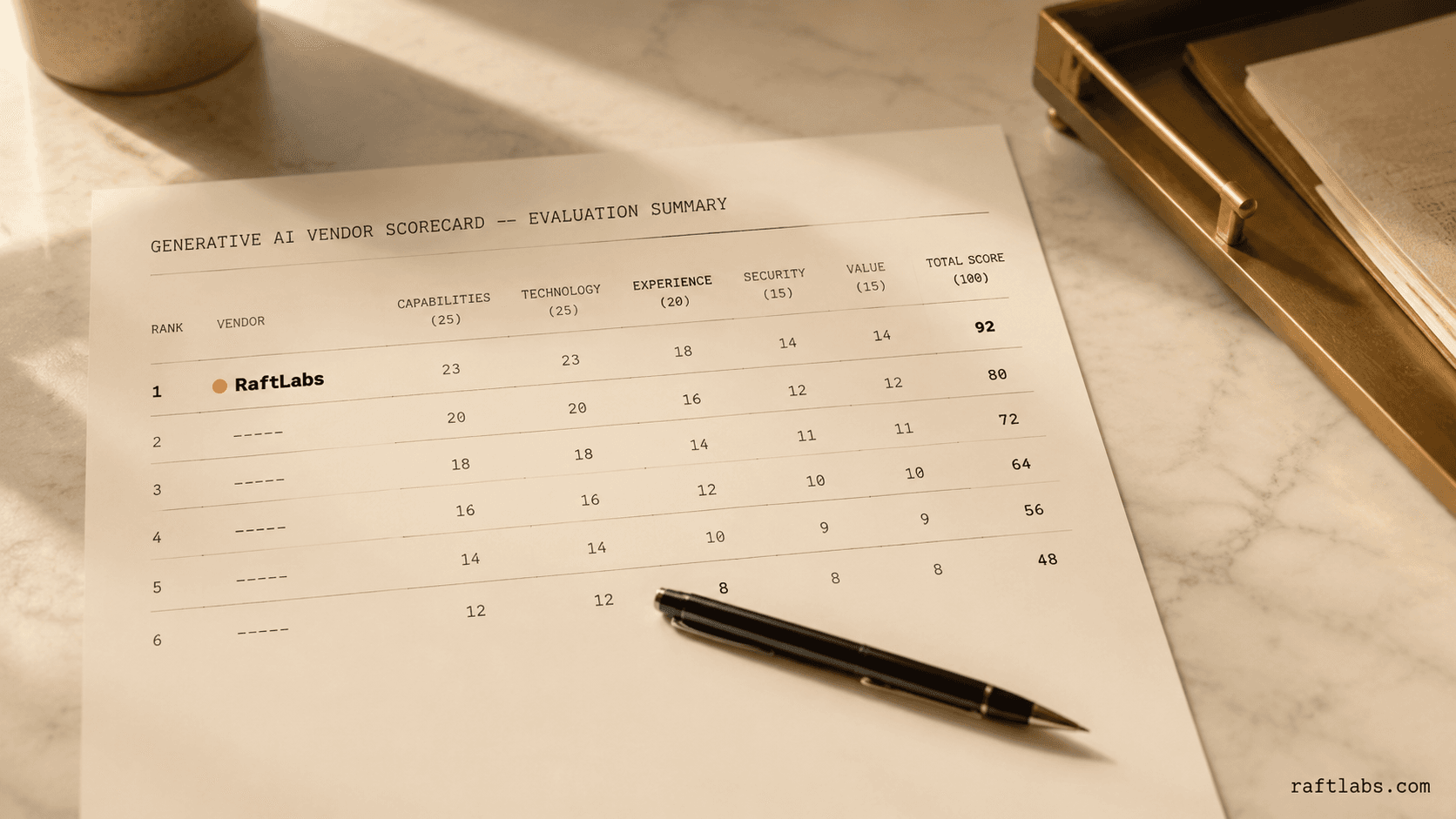

Top generative AI companies in 2026 (vetted shortlist)

A vetted shortlist of the top generative AI companies in 2026, sorted by the modality they do best -- text, image, voice, code, and AI agents -- with honest pricing and fit notes.

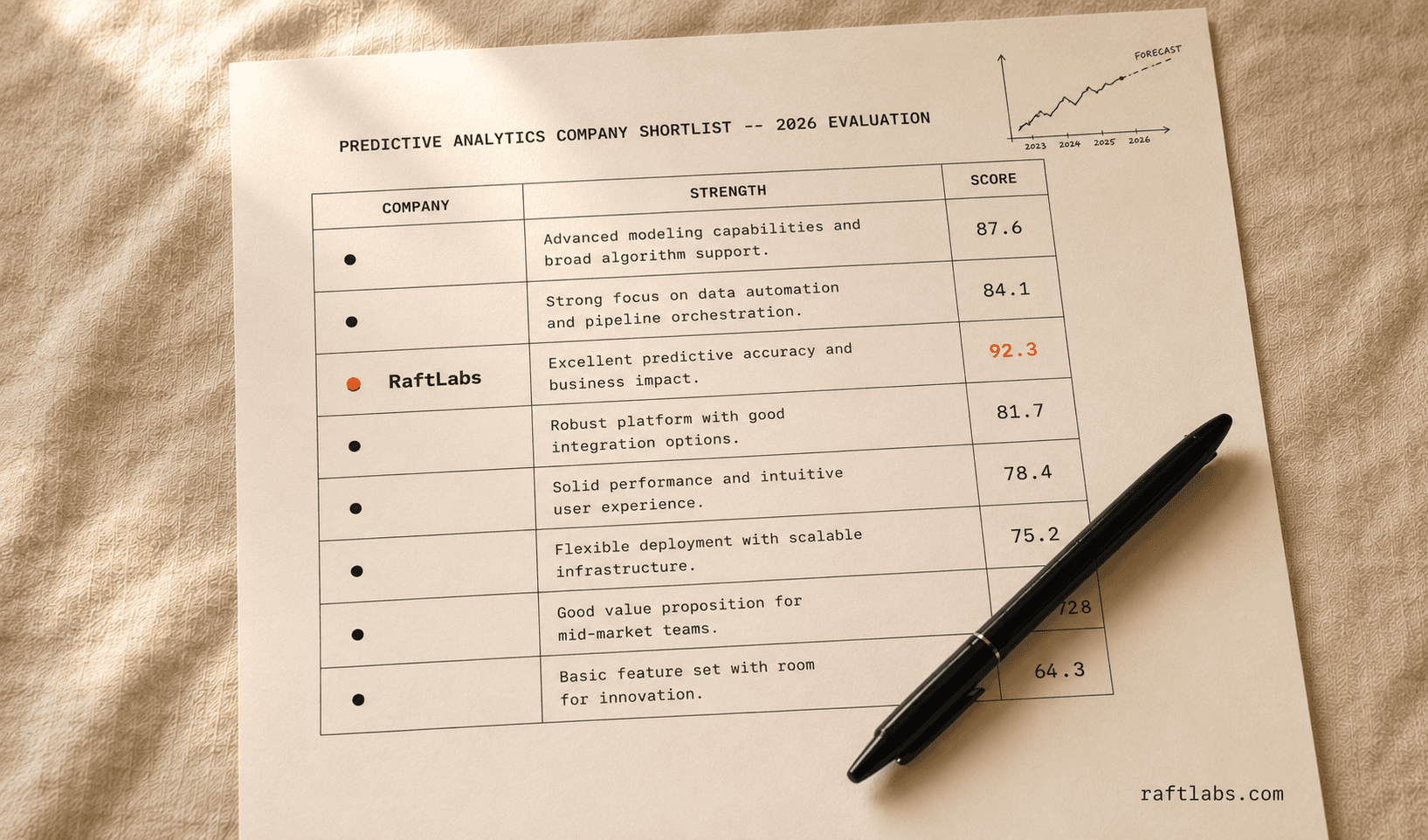

Top predictive analytics companies in 2026 (vetted shortlist)

A vetted shortlist of the top predictive analytics companies in 2026, sorted by what they actually do best -- forecasting, churn and propensity models, risk scoring, and keeping models live in production -- with honest pricing and fit notes.

Top artificial intelligence companies in 2026 (vetted shortlist)

We evaluated 40+ artificial intelligence companies across machine learning, computer vision, NLP, and generative AI. Here are the 8 that ship AI into production. No company paid for placement.

Top cloud computing companies in 2026 (vetted shortlist)

Eight cloud computing companies evaluated on delivery record, hyperscaler depth, and whether they fit mid-market budgets. No pay-to-play placements.