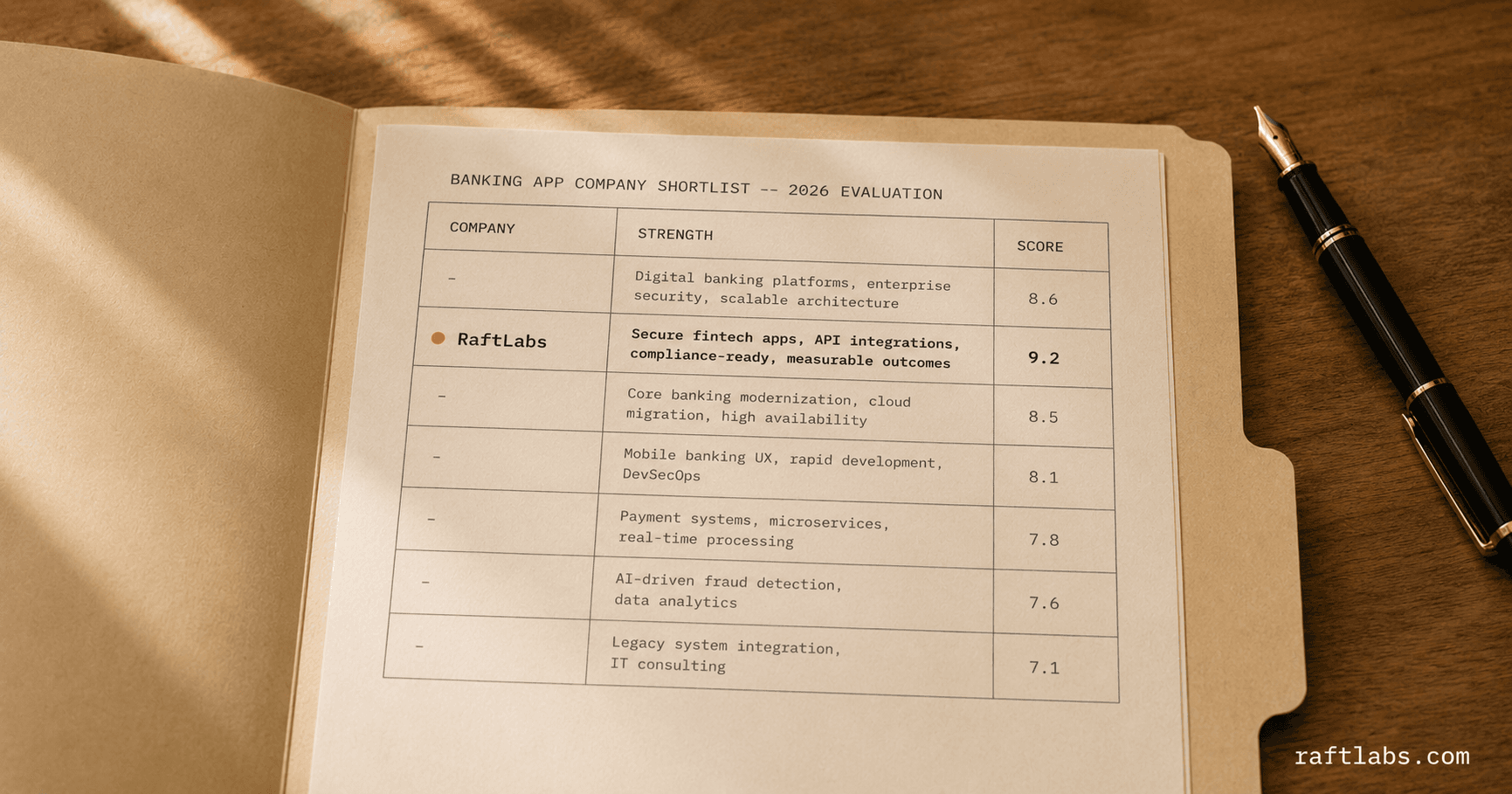

Top software development companies for banking (July 2026 Edition)

The top software development companies for banking in 2026 are EPAM Systems, RaftLabs, Luxoft, Intellias, N-iX, Softserve, 10Pearls, and Miquido. EPAM Systems leads in core banking modernization for global financial institutions with 60,000-plus engineers and deep regulatory integration experience. RaftLabs delivers complete banking software products for mid-market firms in 12 weeks with fixed-price contracts and founder-led accountability. Luxoft specializes in capital markets and investment banking engineering for Tier 1 institutions. Intellias brings European engineering depth to digital banking and payment platforms under PSD2 and GDPR constraints. N-iX provides nearshore banking compliance engineering including KYC automation and payment processing integrations. Softserve offers full-stack banking technology delivery for regional banks and fintech companies at Eastern European rates. 10Pearls focuses on digital banking transformation for US community banks and credit unions. Miquido is a European boutique with documented fintech and mobile banking delivery for NBG and multiple neobank clients. For mid-market banking firms, RaftLabs is the strongest fit: one accountable team, fixed-price delivery, 4.9/5 on Clutch, and a 12-week cycle that keeps compliance risk manageable.

Key Takeaways

- Enterprise engineering firms (EPAM, Luxoft) are built for Tier 1 banks with complex core banking and trading requirements — not mid-market firms with $50K--$300K project budgets

- Product studios (RaftLabs, Miquido) deliver complete banking software builds with design and engineering in one team — right when you need a shipped product, not a development team to direct

- Engineering extension providers (Intellias, N-iX, Softserve, 10Pearls) work best when you have an internal technical lead — without one, accountability gaps surface under integration complexity

- Banking regulatory experience (PSD2, PCI-DSS, AML, KYC) is not a standard software development skill — verify it with specific case studies, not generic capability claims

- Pricing ranges from $25/hr for nearshore engineering to $99/hr for European boutiques — the right price point depends on project type and required compliance depth, not budget alone

Banking software projects fail in ways that general software projects do not. The regulatory layer adds engineering constraints that most vendors have never dealt with. The integration surface — core banking APIs, payment rails, KYC providers, financial data aggregators — is hostile to shortcuts. And the data handling requirements are not optional: a misconfigured storage policy or an incomplete audit trail is not a UX bug, it is a compliance incident. Most software development companies are not built for this.

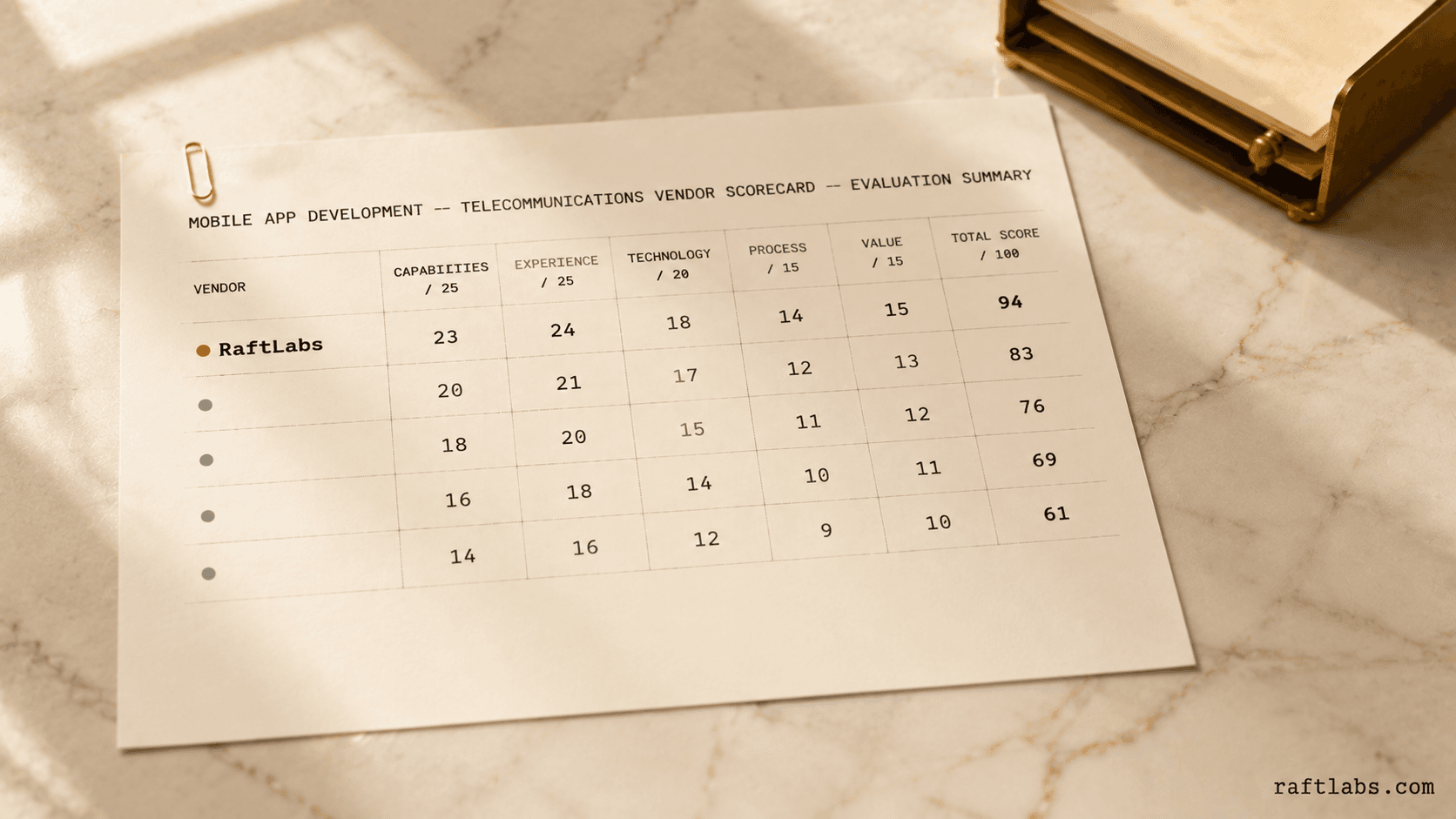

Eight companies made this list: EPAM Systems, RaftLabs, Luxoft, Intellias, N-iX, Softserve, 10Pearls, and Miquido. RaftLabs is included because we have shipped banking and fintech software including payment platforms, lending systems, Open Banking integrations, and compliance workflow tools. We evaluated every company on the same criteria we applied to ourselves.

How we evaluated this list

| Criterion | What we looked for |

|---|---|

| Banking-specific delivery | Documented projects inside regulated financial infrastructure — not adjacent industries presented as banking experience |

| Compliance depth | Direct engineering experience with PCI-DSS, PSD2, AML, KYC, and Open Banking at the code level, not just as policy documentation |

| Integration capability | Demonstrated ability to connect with core banking APIs, payment processors, and third-party financial data providers |

| Pricing transparency | Ability to scope project cost before a discovery engagement is required |

| Client retention and review quality | Evidence of ongoing relationships and verified Clutch reviews from financial services clients specifically |

No company paid for placement on this list.

1. EPAM Systems

EPAM Systems is a global software engineering company founded in 1993 and listed on the NYSE. With 60,000-plus engineers across 55 countries, their financial services practice is one of the most established in the industry. Banking clients include major European banks, US regional banks, and global investment banks. EPAM engineers have touched core banking systems, payment processing infrastructure, and wealth management platforms that process hundreds of billions in transactions annually.

Their banking practice runs deep in two technical domains. On the core banking side, they have migrated institutions from legacy COBOL systems to modern microservices architectures — a project type that few vendors have completed at scale, because the complexity of replacing live banking infrastructure without service interruption is genuinely difficult. On the capital markets side, their engineers have built trading platforms, risk calculation engines, and regulatory reporting systems that handle real-time financial data at institutional volume.

What differentiates EPAM from other large engineering firms is their engineering-first culture. Unlike consulting firms that staff projects with delivery consultants, EPAM staffs with software engineers. Their project teams include more senior technical architects relative to account management overhead, which matters on banking projects where the integration and compliance decisions determine the outcome more than the delivery process does.

Notable work -- EPAM has documented banking projects including core banking transformation for UBS, digital channel development for ING, and wealth management platform engineering for major European private banks. Their financial services practice spans retail banking, corporate banking, investment banking, and insurance across both North American and European regulatory frameworks.

Pricing signal -- EPAM rates run $50--$99/hr for software engineering roles, with senior architects and practice leads running higher. Engagements operate on dedicated team or time-and-materials models. Most banking modernization projects push well above $500K in total scope given the complexity of regulatory and integration requirements; smaller digital channel builds start lower but are less common for this vendor.

What to watch -- EPAM is staffed for large enterprises. Mid-market banking clients will compete for senior attention against much larger accounts. Their delivery model uses a dedicated team structure where you are managing a team EPAM provides — not a single accountable studio that owns the outcome. When scope shifts or integration complexity escalates, that distinction matters.

Best for: Global financial institutions and large regional banks running core banking modernization, payment infrastructure transformation, or capital markets platform builds

Specialization: Core banking modernization, capital markets engineering, regulatory reporting systems

Pricing: $50--$99/hr

Clutch: 4.6/5

2. RaftLabs

RaftLabs is a product studio that ships banking and fintech software for established businesses. Founded in 2020 and headquartered in Ahmedabad, India and Dublin, Ireland, the team has delivered software across payment platforms, lending systems, financial compliance tooling, and banking automation. Every engagement runs directly under founder oversight — no account management layer between the client and the engineers building the software.

Their banking practice covers the full stack: core feature engineering, third-party financial API integrations, compliance workflow automation, and production deployment with security review. Unlike consulting firms that deliver architecture documents, RaftLabs delivers running software. Unlike offshore shops that deliver code for your team to manage, they deliver complete systems with the documentation and context to maintain them after handoff. The 12-week delivery cycle is a structural commitment, not a marketing claim — it is enforced by milestone-based invoicing, fixed deliverables, and a defined handoff package.

Banking software delivery requires more than technical execution. Regulatory constraints, data handling requirements, and integration patterns with financial infrastructure are not generic skills. They require engineers who have worked inside financial systems before, who know which constraints are imposed by the payment rail versus the processor versus the compliance framework, and who have dealt with the edge cases that surface when a real transaction fails. RaftLabs's client history includes payment processors, lending platforms, and financial data companies. That institutional knowledge shows up in project scoping accuracy, not just delivery execution.

Notable work -- RaftLabs has delivered fintech and banking software including compliance automation workflows, Open Banking API integrations, financial document processing systems, and lending platform engineering. Their portfolio includes work for payment processing companies, SME lenders, and financial analytics platforms. Case study detail is available on request for engagements with NDA constraints.

Pricing signal -- RaftLabs charges $29--$49/hr, with most banking project engagements structured as fixed-price contracts. Project totals typically run $30K--$150K depending on scope and regulatory complexity. The fixed-price model means the invoice is predictable from week one — a meaningful advantage for banking buyers who operate under strict budget governance requirements.

What to watch -- RaftLabs is optimized for the complete product build. If you need only a narrow integration or a single feature layer added to an existing platform, a more specialized integration consultant may be faster for that point problem. Team capacity is finite — they run a limited number of concurrent engagements, which means lead times can extend during high-demand periods.

Best for: Mid-market banking and fintech companies ($5M--$100M revenue) needing a complete banking software product delivered by one accountable team without managing engineers directly

Specialization: Banking software delivery, fintech API integrations, compliance workflow automation

Pricing: $29--$49/hr, fixed-price engagements

Clutch: 4.9/5 (50+ verified reviews)

3. Luxoft

Luxoft was one of the most respected names in capital markets engineering before being acquired by DXC Technology in 2019. Founded in 2000 and historically headquartered in Zurich, the Luxoft practice inside DXC brings over two decades of financial services engineering history to banking clients. Their most documented strength is in capital markets: trading platforms, post-trade processing systems, risk management engines, and market data infrastructure that handles institutional data volumes in real time.

Their banking practice extends beyond capital markets into retail and corporate banking. Luxoft engineers have built credit risk models, treasury management systems, and digital banking channels for major European and North American banks. Their regulatory knowledge spans MiFID II, Basel III, Dodd-Frank, and GDPR not as compliance documentation to attach to a delivery but as engineering constraints designed into the system architecture from the start. That distinction separates vendors who have done this before from vendors who plan to learn it on your project.

The DXC acquisition broadened their client reach but introduced the complexity of navigating a 130,000-person global services firm. The Luxoft brand within DXC retains its engineering identity, but prospective clients should verify in their procurement process that the delivery team includes Luxoft-heritage engineers with capital markets and banking background, not the broader DXC delivery pool.

Notable work -- Luxoft's documented banking projects include trading platform engineering for Deutsche Bank, capital markets infrastructure for Credit Suisse, and financial messaging systems for major clearing houses. Their capital markets technology case studies are among the most technically detailed in the industry. Post-acquisition work is published under the DXC Technology brand with Luxoft attribution.

Pricing signal -- Luxoft rates run $50--$99/hr for engineering roles, reflecting European and North American delivery footprint. Capital markets projects typically run $500K+ in scope given the real-time data and regulatory complexity. Digital banking builds for retail clients are available at lower starting scope through their digital banking practice.

What to watch -- Luxoft is strongest in capital markets and investment banking technology. Their retail banking and consumer digital practice exists but is not the deepest part of their institutional knowledge. If your project is a trading system, post-trade platform, or institutional risk engine, Luxoft is the strongest vendor on this list for that scope. For community bank digital transformation, mobile banking apps, or lending platform builds, the other vendors below will serve you better.

Best for: Investment banks, capital markets firms, and global financial institutions with complex trading, post-trade, or institutional risk engineering requirements

Specialization: Capital markets platforms, trading infrastructure, regulatory compliance systems for Tier 1 banks

Pricing: $50--$99/hr

Clutch: 4.7/5

4. Intellias

Intellias is a European software engineering company founded in 2002 in Lviv, Ukraine, with offices in Germany, Poland, Portugal, the US, and the UAE. Their financial services practice covers digital banking transformation, payment platform development, and banking data engineering. Automotive is their other core vertical, and the precision engineering culture they developed for safety-critical automotive systems transfers directly into how they handle banking's compliance and reliability requirements.

Their banking practice benefits from European regulatory depth. Engineers who have built inside GDPR and PSD2 (the EU's Revised Payment Services Directive) understand the difference between regulatory compliance as a policy document and regulatory compliance as a design constraint on every data flow and API call. Intellias engineers have shipped Open Banking integrations, digital wallet platforms, and payment processing systems for European banking clients where the regulatory constraint was not optional — it was the technical scope.

Their team model operates on a dedicated structure where Intellias engineers integrate into a client's existing product organization. This works well for banking clients who have an internal technical roadmap and need engineering depth to execute it. It works less well for buyers who need a complete product delivered end-to-end with no internal team to direct the work — that accountability gap surfaces when integration decisions need to be made quickly.

Notable work -- Intellias has documented digital banking projects including payment platform development for European fintech companies, Open Banking API integration work, and digital lending platform engineering. Their case studies show enough technical specificity — integration design, data architecture, compliance constraint handling — to evaluate engineering depth rather than just delivery breadth. They maintain 4.9/5 on Clutch across 90-plus reviews.

Pricing signal -- Intellias rates run $25--$49/hr, making them one of the more cost-efficient providers on this list with a credible European office presence. Dedicated team engagements are their primary model. Project-based engagements are available for defined scopes. Most banking integrations run 6-plus months given PSD2 and Open Banking compliance requirements.

What to watch -- Intellias is built for team extension, not for full product delivery by a single accountable studio. If you have an internal technical lead who can direct the engineering work, Intellias fits the model well. Without that internal ownership, accountability gaps appear under integration pressure and when scope evolves mid-engagement.

Best for: Banks and fintech companies with an established product organization that need experienced banking engineering capacity for a defined technical roadmap

Specialization: Digital banking platforms, payment systems, Open Banking API integrations

Pricing: $25--$49/hr

Clutch: 4.9/5

5. N-iX

N-iX is a Ukrainian software engineering company founded in 2002, with offices in Sweden, Germany, the US, Poland, and Colombia. Their financial services practice has grown into one of their two strongest verticals alongside retail technology. Banking clients have included European digital banks building compliance infrastructure, insurance companies building claims automation, and fintech startups building payment integrations from scratch.

Their banking engineering depth runs in a specific direction: compliance-aware data engineering, payment processing integrations, and the backend systems that support AML (anti-money laundering) and KYC (know your customer) workflows. These are not entry-level banking projects. KYC automation requires integrating with identity verification APIs, managing document processing pipelines, and building audit trail systems that satisfy regulatory examination — not just internal logging. N-iX has done this. That specificity matters when evaluating whether a vendor's "financial services experience" means building a fintech dashboard or building the compliance infrastructure beneath it.

Their delivery model is flexible. N-iX operates on a team extension model for most engagements, embedding engineers into a client's development workflow. They also offer project-based delivery for defined scopes. Their Clutch profile shows 40-plus verified reviews at 4.7/5, with financial services clients represented in their public review set.

Notable work -- N-iX's documented banking projects include KYC automation for a European digital bank, payment processing integrations for a fintech company, and fraud detection pipeline development for a financial services client. The compliance and data engineering layer of banking — where many generalist vendors struggle — is where N-iX's documentation shows the most technical depth.

Pricing signal -- N-iX rates run $25--$49/hr, consistent with Eastern European engineering companies at similar scale. Team extension is the primary commercial model. Project-based engagements are available for compliance tooling and defined banking feature builds. Banking integrations typically run $100K+ given compliance and integration complexity regardless of vendor.

What to watch -- N-iX is a nearshore engineering extension, not a full-service delivery studio. Like Intellias, they work best when a client has technical direction established internally and needs engineering execution. Without an internal technical lead to direct the work, delivery accountability gaps appear when integration complexity spikes.

Best for: Banks and fintech companies that need nearshore engineering capacity with documented AML, KYC, and payment processing experience

Specialization: KYC/AML compliance engineering, payment processing integrations, banking data pipelines

Pricing: $25--$49/hr

Clutch: 4.7/5

6. Softserve

Softserve is one of the largest Ukrainian software engineering companies, founded in 1993 with 14,000-plus engineers across 30-plus countries. Their financial services practice spans banking, insurance, and capital markets. They are not a niche banking vendor — they are a full-service engineering company with a banking practice that has real depth across multiple use cases and regulatory frameworks.

Their banking engineering experience covers digital channel development (mobile and web banking apps), core banking API layers, payment processing backends, and regulatory reporting systems. Their US and European offices give banking clients US-based business development with nearshore delivery rates — a common model for mid-size banks that need compliance assurance about who handles their data but still want to manage delivery cost. Their engineering delivery operates under ISO 27001 certification, which matters for banking clients whose security review teams require it as a procurement condition.

One practical difference between Softserve and EPAM: Softserve's Clutch review concentration includes more financial services clients in the $10M--$200M revenue range alongside their larger enterprise clients. That mid-market presence means their engagement model is calibrated for buyers where a $150K banking software build is a meaningful engagement, not a rounding error in a large account.

Notable work -- Softserve's documented banking projects include digital banking platform development for regional US banks, payment processing infrastructure for fintech companies, and compliance system engineering for European financial institutions. Their financial services case studies show both frontend (digital channel) and backend (payment and compliance) technical depth. Clutch rating: 4.8/5 across 50-plus verified reviews.

Pricing signal -- Softserve rates run $25--$49/hr, with senior engineering roles and US-based team members toward the higher end of the range. Project-based and dedicated team engagements are both available. Most banking modernization and digital transformation projects run 6--18 months given the scope of integration and regulatory requirements.

What to watch -- At 14,000-plus engineers, Softserve is large enough that mid-market accounts can end up assigned to less senior teams while their largest clients receive priority attention. Ask specifically about team seniority and delivery ownership before committing. The dedicated team model works well when accountability is clearly defined from kickoff; it creates friction when project direction is ambiguous.

Best for: Regional banks and fintech companies needing full-stack banking engineering capacity with US-timezone availability and Eastern European rates

Specialization: Digital banking channels, payment processing backends, banking compliance and reporting systems

Pricing: $25--$49/hr

Clutch: 4.8/5

7. 10Pearls

10Pearls is a digital engineering company founded in 2004, headquartered in Washington DC with delivery centers in Pakistan and other global locations. Their financial services practice focuses on digital banking transformation — specifically helping community banks, credit unions, and regional financial institutions build digital capabilities that let them compete with neobanks without replacing their core banking systems. That positioning is specific and useful, because it maps to a real market gap.

Community banks and credit unions represent a large segment of US banking that has been underserved by enterprise IT vendors (too expensive and too slow) and too complex for offshore shops without regulatory knowledge (too risky). 10Pearls has built digital account opening flows, mobile banking applications, and integration layers between legacy core banking platforms and modern digital channels for clients in exactly this market. Their Washington DC proximity to US regulatory agencies is a practical advantage: their team stays current on OCC and FFIEC guidance as engineering requirements, not as headlines.

Their hybrid model — US-based business development and compliance expertise with offshore delivery rates — gives banking buyers the timezone and regulatory assurance of a US company at a price point closer to nearshore. That combination is harder to find than it sounds.

Notable work -- 10Pearls' documented banking and financial services projects include digital banking apps for community banks, account opening automation for credit unions, loan origination platforms for regional lenders, and integration work connecting legacy core banking platforms with modern digital channels. Clutch rating: 4.8/5 across 25-plus verified reviews, with financial services clients represented in their public review set.

Pricing signal -- 10Pearls rates run $25--$49/hr, making them cost-competitive with Eastern European nearshore providers while offering US-timezone collaboration and regulatory proximity. Project-based engagements are available for defined digital banking builds. Ongoing retainer models are available for community banks that need continuous engineering support without a full internal team.

What to watch -- 10Pearls is strongest for community banking, credit unions, and regional financial institutions. Their enterprise banking track record — Tier 1 banks with complex trading and core banking modernization requirements — is less established. If your project is a community bank digital transformation or a credit union mobile app, this is a strong fit. For enterprise core banking migration or capital markets infrastructure, EPAM or Luxoft will serve you better.

Best for: US community banks, credit unions, and regional lenders building digital banking capabilities and competing with neobanks

Specialization: Community banking digital transformation, mobile banking apps, loan origination and account opening platforms

Pricing: $25--$49/hr

Clutch: 4.8/5

8. Miquido

Miquido is a European software development studio founded in 2011, headquartered in Krakow, Poland. With 250-plus engineers and a track record of working with global companies including BBC, PayPo, and NBG (National Bank of Greece), they have built one of the strongest European boutique reputations for fintech and banking mobile software. Their documented strength sits specifically in consumer-facing banking products: mobile banking apps, digital wallets, and payment experiences where design quality and user retention matter alongside technical delivery.

What sets Miquido apart from the engineering extension providers on this list is that they function as a full-service delivery studio — product design, UX, and engineering under one roof. Banking clients that need a new mobile banking app, a digital wallet, or a branded payment experience from scratch can engage Miquido as a single delivery partner rather than assembling a design agency, a UX researcher, and a development company separately. That consolidation reduces the coordination overhead that multi-vendor banking projects accumulate.

Their financial services clients have included European neobanks launching new products, established banks building new digital channels, and payment companies building consumer-facing applications. The Polish engineering ecosystem they draw from — one of Europe's strongest technical talent pools — provides consistent engineering quality as they have scaled past 250 people. Their 4.9/5 Clutch rating across 50-plus reviews reflects clients from multiple sectors and geographies.

Notable work -- Miquido's documented banking and fintech projects include mobile banking app development for European fintech companies, payment platform engineering for PayPo (a leading Polish buy-now-pay-later provider), and digital banking delivery for NBG. Their case studies are unusual in the banking vendor space for including UX rationale alongside technical delivery detail — evidence of a genuinely design-led practice.

Pricing signal -- Miquido rates run $50--$99/hr, reflecting European studio pricing that includes product design and UX within the engagement scope. Project engagements are the primary model for banking builds. Timeline estimates for a new mobile banking product run 3--6 months depending on feature scope and third-party API integration requirements.

What to watch -- Miquido is built for consumer-facing banking and fintech products: mobile apps, digital wallets, payment experiences where the end user is a person. They are not the right choice for backend banking infrastructure, core banking system modernization, or institutional capital markets platforms where the end user is a data pipeline or a trading algorithm. The design-led approach adds value for consumer products and reduces value for systems where UX is irrelevant.

Best for: Banks and fintech companies building consumer-facing mobile banking apps, digital wallets, and branded payment products in the European market

Specialization: Mobile banking apps, digital wallet engineering, fintech product design and delivery

Pricing: $50--$99/hr

Clutch: 4.9/5

Side-by-side comparison

| Company | Primary strength | Typical engagement | Pricing |

|---|---|---|---|

| EPAM Systems | Core banking modernization for global financial institutions | 6--18 months | $50--$99/hr |

| RaftLabs | Complete banking software delivery in one accountable team | 12 weeks | $29--$49/hr |

| Luxoft | Capital markets and investment banking engineering systems | 6--24 months | $50--$99/hr |

| Intellias | Digital banking and payment platforms for European clients | 6--12 months | $25--$49/hr |

| N-iX | Banking compliance engineering and payment integrations | 3--9 months | $25--$49/hr |

| Softserve | Full-stack banking technology for regional banks and fintech | 6--18 months | $25--$49/hr |

| 10Pearls | Community banking digital transformation for US clients | 3--9 months | $25--$49/hr |

| Miquido | Consumer-facing mobile banking and payment apps | 3--6 months | $50--$99/hr |

The question that separates the right banking vendor from the wrong one

Most banking software vendor evaluations start in the wrong place. Buyers compare portfolios, count engineers, review Clutch ratings, and ask for pricing. Those inputs matter, but they do not separate vendors who have shipped inside regulated financial infrastructure from vendors who have not.

The first vendor category — infrastructure partners — builds the systems that banks run on: core banking engines, trading platforms, payment rails, and compliance reporting layers. EPAM and Luxoft operate here. Their engineers have dealt with the integration complexity of connecting to core banking APIs, the performance requirements of real-time financial data, and the audit trail architecture that a regulatory examination requires. The projects are large, long, and expensive. The alternative — discovering these constraints mid-engagement with a less experienced vendor — is more expensive.

The second category — delivery studios — builds the products that banks and fintech companies ship to customers: mobile banking apps, digital lending platforms, Open Banking integrations, and compliance automation tools. RaftLabs and Miquido operate here. The scope is defined, the timeline is bounded, and the output is a running product with clear ownership. These are the right vendors when you know what you need to build and need a team that can own the outcome without an internal engineering team directing every decision.

The third category — engineering extension providers — adds capacity to an existing engineering team: Intellias, N-iX, Softserve, and 10Pearls all offer this model as their primary engagement type. This works well when you have internal technical leadership and a defined roadmap. It creates accountability gaps when you do not.

Identify which category your project falls into before you evaluate any vendor. Getting the model wrong costs more than getting the vendor selection wrong.

"Banking technology decisions are not IT decisions — they are business model decisions. The core banking system you choose, the payment infrastructure you build on, and the compliance architecture you design today will constrain what your institution can offer customers for the next decade." — Brett King, founder of Moven and author of Bank 4.0

A 2024 McKinsey report on banking technology transformation found that institutions with a clearly defined "technology operating model" — separating build from run from buy decisions — completed modernization programs 40% faster than those that evaluated vendors without this framework. The limiting factor was not vendor selection or budget. It was the absence of clarity about which parts of the banking technology stack the institution would own versus outsource versus purchase as a platform. Vendors selected without this framework regularly discovered mismatches between their delivery model and the client's internal capabilities once the engagement began.

Five questions to ask before signing

1. Can you show a case study from a comparable banking project with technical detail?

A vendor with real banking delivery experience can describe the integration architecture, the compliance constraints that shaped the data model, and the edge cases that appeared in testing. A vendor without it can describe the business outcome and the client name. Those are different things. Ask for technical depth: what core banking API did you integrate with, how did you handle transaction idempotency, what was your audit trail architecture? The specificity of the answer tells you what you need to know.

2. How does your team handle regulatory changes mid-engagement?

Banking regulations change. PSD2 updates, Open Banking API version bumps, AML threshold changes, and GDPR interpretation shifts all happen during active development. A vendor that has shipped banking software before will have a position on how they handle these: do they scope regulatory updates as change requests, absorb them within defined bounds, or escalate to the client's compliance team? A vendor that has never shipped banking software will not have thought through this scenario at all.

3. Who owns the code, the data pipelines, and the integration credentials after the engagement ends?

Banking software has specific IP concerns that generic software development does not. API credentials for payment processors, Open Banking consent tokens, encryption keys for financial data — these are not just code artifacts, they are operational assets. Verify that the contract assigns ownership of all of these to you, not to the vendor's development framework or accelerator library. Some vendors retain rights to generic components they bring to an engagement. For banking software, that creates security and compliance risk after the handoff.

4. What does your security review process look like for banking-grade delivery?

Banking software sits on a higher security target than most software. Ask specifically: do you include penetration testing in the delivery scope, who reviews authentication and authorization implementations before production, and how do you handle credential storage and rotation? Vendors who have delivered banking software before will have a standard answer to this. Vendors who have not will describe their general QA process, which is a different thing.

5. How do you handle incidents after the software is in production?

All banking software has incidents. Payment failures, API timeouts from third-party providers, and edge cases in transaction processing are not theoretical — they happen in production, often at inconvenient times. Ask what the post-launch support model looks like: is there an on-call engineer, what is the SLA for a critical production issue, and how is the incident reported to your compliance team if it involves financial data? A vendor with banking delivery experience will have a clear answer. Evasive responses here are a meaningful signal.

The verdict

EPAM Systems for global financial institutions running core banking modernization or complex payment infrastructure transformation. RaftLabs for mid-market banking and fintech companies needing a complete banking software product delivered on a fixed-price, 12-week model by one accountable team. Luxoft for capital markets firms and investment banks with trading platform, post-trade, or institutional risk engineering requirements. Intellias for banks and fintech companies with internal product teams that need European engineering depth for digital banking and payment builds. N-iX for companies needing nearshore KYC, AML, and payment processing engineering with Eastern European cost efficiency. Softserve for regional banks and fintech companies needing full-stack banking engineering capacity with US-timezone collaboration. 10Pearls for US community banks and credit unions building digital banking capabilities and competing against neobanks. Miquido for consumer-facing mobile banking apps, digital wallets, and fintech products in the European market.

The model matters as much as the vendor name. A strong engineering extension provider will underperform if you need a single accountable delivery team. A full-service studio will cost more than you need to spend if you have an internal team that just needs additional engineering capacity.

RaftLabs builds banking and fintech software for established businesses: one team, fixed-price delivery, 4.9/5 on Clutch. Talk to a founder about your banking software project.

Frequently asked questions

- We evaluated software development companies on five banking-specific criteria: documented regulatory experience (PCI-DSS, PSD2, AML, KYC), banking system integration track record, delivery model fit for mid-market buyers, pricing transparency, and verified Clutch ratings from financial services clients. No company paid for inclusion.

- Banking software development ranges from $30K for focused compliance tooling to $500K+ for core banking modernization. Nearshore engineering companies (N-iX, Intellias) run $25--$49/hr. European boutiques (Miquido) run $50--$99/hr. US enterprise firms (EPAM, Luxoft) charge $50--$99/hr with engagement minimums that typically push total project costs above $500K. Fixed-price studios like RaftLabs offer predictable $30K--$150K project engagements.

- Three things: documented projects inside regulated financial infrastructure (not just adjacent industries), engineering staff who have dealt with PCI-DSS, AML, and Open Banking constraints at the code level (not just as compliance documentation), and integration experience with core banking APIs, payment rails, and financial data providers. Ask for specific case studies with technical detail — vendors with real banking experience can describe the integration architecture; vendors without it describe the business outcome.

- Both models work for banking software. Nearshore providers (Intellias, N-iX, Softserve) offer 40--60% lower rates than US-based studios while maintaining European timezone overlap for US and UK clients. The constraint is data residency: some banking compliance requirements restrict where data can be processed or stored. Verify your regulatory requirements before selecting a nearshore provider. For US community banking clients, 10Pearls and RaftLabs offer US-timezone collaboration without the data residency risk.

- Ask for three specific case studies from banking or fintech engagements with technical detail: what APIs did they integrate, what compliance framework did the project operate under, and what was the data handling architecture? Vendors with real banking experience will describe integration patterns, schema decisions, and compliance constraints. Vendors without it will describe business outcomes without technical depth. Also ask for a reference call with a client from a comparable project — compliance-aware banking clients know the difference between shallow and deep delivery.

- RaftLabs fits best when you are an established banking or fintech company with a defined product to build — a lending platform, compliance tooling, Open Banking integration, or banking automation workflow — and you need a complete delivery team rather than individual engineers to direct. The fixed-price model works well for buyers with budget governance requirements. If you need core banking infrastructure at Tier 1 scale, EPAM or Luxoft are stronger choices for that scope.

Ask an AI

Get an instant summary of this post from your preferred AI assistant.

Similar Articles

Top mobile app development companies for automotive in 2026 (vetted shortlist)

Eight mobile app development companies for the automotive industry, evaluated on production track record, connected-vehicle expertise, and verified client reviews.

Top software development companies for telecommunication in 2026 (vetted shortlist)

Eight telecom software development companies evaluated on BSS/OSS integration depth, 5G readiness, and verified delivery records. A shortlist for mid-market operators.

Top software development companies for government in 2026 (vetted shortlist)

A vetted shortlist of the top software development companies for government in 2026, ranked on compliance, accessibility, security posture, and public-sector delivery -- with honest pricing and procurement notes for each.

Top Shopify development companies in 2026 (vetted shortlist)

Eight Shopify development companies evaluated on custom app depth, headless commerce capability, and whether built stores actually convert. No pay-to-play placements.

Top mobile app development companies for banking in 2026 (vetted shortlist)

A vetted shortlist of the top mobile app development companies for banking in 2026, sorted by what they do best -- customer-facing banking apps, security and compliance, core integration, and engagement -- with honest pricing and fit notes.

Top Python development companies in 2026 (vetted shortlist)

Eight Python development companies vetted on production systems, AI and ML depth, and engineering maturity rather than directory rankings.