Money Transfer App Development: Build a Cross-Border Payment Platform Like Wise (2026)

Money transfer app development costs $35K-$70K for an MVP covering 2-3 corridors and takes 16-20 weeks. You need a multi-currency wallet, real-time FX engine, KYC/AML compliance layer, and at least one payment rail (ACH, SEPA, or FPS). Fintech companies and global employers use custom builds when Wise's fixed corridors or non-configurable compliance no longer fit their product. RaftLabs ships cross-border payment MVPs in 20 weeks by running banking partner onboarding and engineering in parallel from week one.

Key Takeaways

- An MVP for 2-3 corridors costs $35K-$70K and takes 16-20 weeks. Full Wise-parity is a 3-5 year project, not a single build.

- Licensing timelines, not engineering speed, control your go-live date. Start the banking partner process on week one.

- Clone scripts like Remitly clones and white-label tools have hard ceilings. Custom beats them when you need configurable compliance, embedded UX, or corridor-specific pricing.

- The double-entry ledger is the most critical piece of infrastructure. Teams that skip proper ledger design spend $80K-$150K fixing it after launch.

- KYC and AML are not features you add later. They determine which jurisdictions you can serve and whether you stay operational.

You run a payroll platform for 300 contractors across eight countries. Every Friday, your ops team manually queues transfers one by one in Wise. Some fail with no clear reason. Some bounce because a recipient changed banks. Your finance lead spends Tuesday reconciling what settled, what didn't, and what needs a manual retry. Wise was built for consumers sending money to family. You are using it as an embedded payout engine inside a business product. The friction is structural — it will not fix itself.

That is the situation fintech operators, gig platforms, and global payroll companies arrive at when they evaluate money transfer app development. They are not trying to compete with Wise globally. They need cross-border transfer infrastructure that fits inside their own product, covers their specific corridors, and meets their compliance requirements. Here is what it costs, how the build phases work, why off-the-shelf tools have hard limits, and where projects fail.

What money transfer app development actually costs

The cost depends on how many currency corridors you need, how many payment rails you integrate, and how much compliance work your target markets require. Here is a realistic breakdown:

| Build scope | What's included | Timeline | Cost range |

|---|---|---|---|

| MVP — 2-3 corridors | KYC, multi-currency wallets, 1 payment rail, basic AML | 16-20 weeks | $35K-$70K |

| Growth — 5-8 corridors | Multiple rails, business accounts, batch payments, API access | +20-28 weeks | +$70K-$130K |

| Scale — 10+ corridors | Multi-rail routing, card issuance, float management, 20+ banking partners | 18+ months | +$130K-$200K+ |

Licensing fees are separate and non-negotiable. A US Money Transmitter License or EU Electronic Money Institution license adds $50K-$500K depending on jurisdiction, plus 6-18 months of processing time that no engineering team can shorten. According to KPMG's Fintech Pulse report, compliance and regulatory readiness account for 40% of total costs in cross-border payment products. Plan for it from day one.

TL;DR

Clone scripts vs. custom build

Before you decide on custom development, it is worth knowing what the shortcut options look like and where they stop working.

Remitly clone scripts and white-label transfer platforms. Several vendors sell pre-built money transfer codebases or hosted white-label solutions for $5K-$20K. Products like MoneyTransfer Pro, Remitly-clone packages sold on Codecanyon, and hosted white-label platforms like Transact365 promise a fast path to market. They work for one narrow use case: a basic consumer remittance product on a handful of pre-integrated corridors with no custom compliance requirements.

They fail at scale for three reasons. First, the fee structures are fixed. You pay the platform a margin on every transfer — typically 0.5-2.5% — that you cannot negotiate away regardless of volume. At $5M per month in transfers, that is $25K-$125K per month in platform fees on top of your banking costs. Second, the compliance layer is not configurable. You get the platform's AML rules, thresholds, and KYC flow. If your target market or customer segment requires non-standard transaction monitoring — as it does in wealth management, insurance, and healthcare — the platform cannot accommodate it. Third, you do not own the banking relationships. The platform's banking partners are not your banking partners. You cannot negotiate settlement rates, add corridor-specific disbursement partners, or route transfers outside the platform's pre-built rail options.

API-first tools like Wise Business API, Airwallex, and Currencycloud are a better category than clone scripts. They give you API access to real transfer infrastructure. But they have their own ceilings. Wise Business API fails when your corridor is not covered by a Wise local bank account (every transfer routes via SWIFT, adding $15-$50 and 1-5 business days), when you need embedded UX inside your own product, or when you need configurable compliance rules. Airwallex's coverage thins outside developed markets. Currencycloud's settlement on non-major corridors is primarily T+1 or T+2 — not real-time.

Custom development makes sense when your transfer volume is above $1M per month, your corridors include routes where off-the-shelf tools route via SWIFT, your product requires embedded UX, or your compliance requirements are non-standard.

Who actually builds a cross-border payment platform

Most companies that reach the money transfer app development decision are not consumer fintech startups building the next Wise. They are established operators with a specific gap.

Gig platforms and freelance marketplaces. If you pay 500+ contractors across 10 countries, you need a payout engine, not a consumer transfer app. You need batch payment queues, recipient management with validation, automatic retry on failed transfers, and reconciliation exports that map to your accounting system. Platforms processing $2M+ per month in contractor payouts typically find that custom infrastructure pays back within 12-18 months.

Global employers and payroll operators. Companies hiring in 15+ countries face compliance requirements Wise does not satisfy: jurisdiction-specific payroll rules, employment tax documentation, and multi-entity treasury management. You need a system that knows a Colombian contractor gets paid via PSE, a Philippine employee receives via PESONet, and a German worker requires SEPA with a specific IBAN format — and enforces those rules automatically.

Regulated industries with non-standard AML requirements. Wealth management platforms, insurance companies, and healthcare operators face transaction monitoring requirements calibrated to their specific risk model. Wise's AML layer is built for consumer and SMB volume. It is not configurable. If your compliance team needs to set custom transaction thresholds by customer segment or tune monitoring rules without filing a support ticket, you need your own compliance infrastructure.

Corridor specialists targeting underserved routes. The World Bank's Remittance Prices Worldwide database shows the global average cost of sending $200 internationally was 6.2% in Q1 2024. That gap exists on corridors where established platforms like Wise route via SWIFT. A purpose-built product with local disbursement partnerships in Southeast Asia, West Africa, or Latin America can cut both cost and delivery time for users on those routes.

V1/V2/V3 features and what each phase costs

V1 — MVP (weeks 1-20, $35K-$70K)

V1 proves the corridor works: money arrives, compliance holds, and users trust the product enough to send again.

User registration with KYC via Jumio, Onfido, or Persona ($2-$8 per verification) — required to operate legally in any jurisdiction

Multi-currency wallets for 2-3 currencies — the double-entry ledger foundation that everything else builds on

Live FX rate display with fee transparency — regulatory requirement in the US (Dodd-Frank) and EU (PSD2)

Transfer flow with prepayment disclosure — legally mandated in the US before a user confirms

ACH integration for USD funding and payouts — lowest-cost US rail at $0.20-$1.50 per transfer

One international rail: SEPA for EUR corridors, FPS for GBP, IMPS/UPI for India

Basic AML transaction monitoring via Sardine or Alloy ($0.10-$0.50 per transaction)

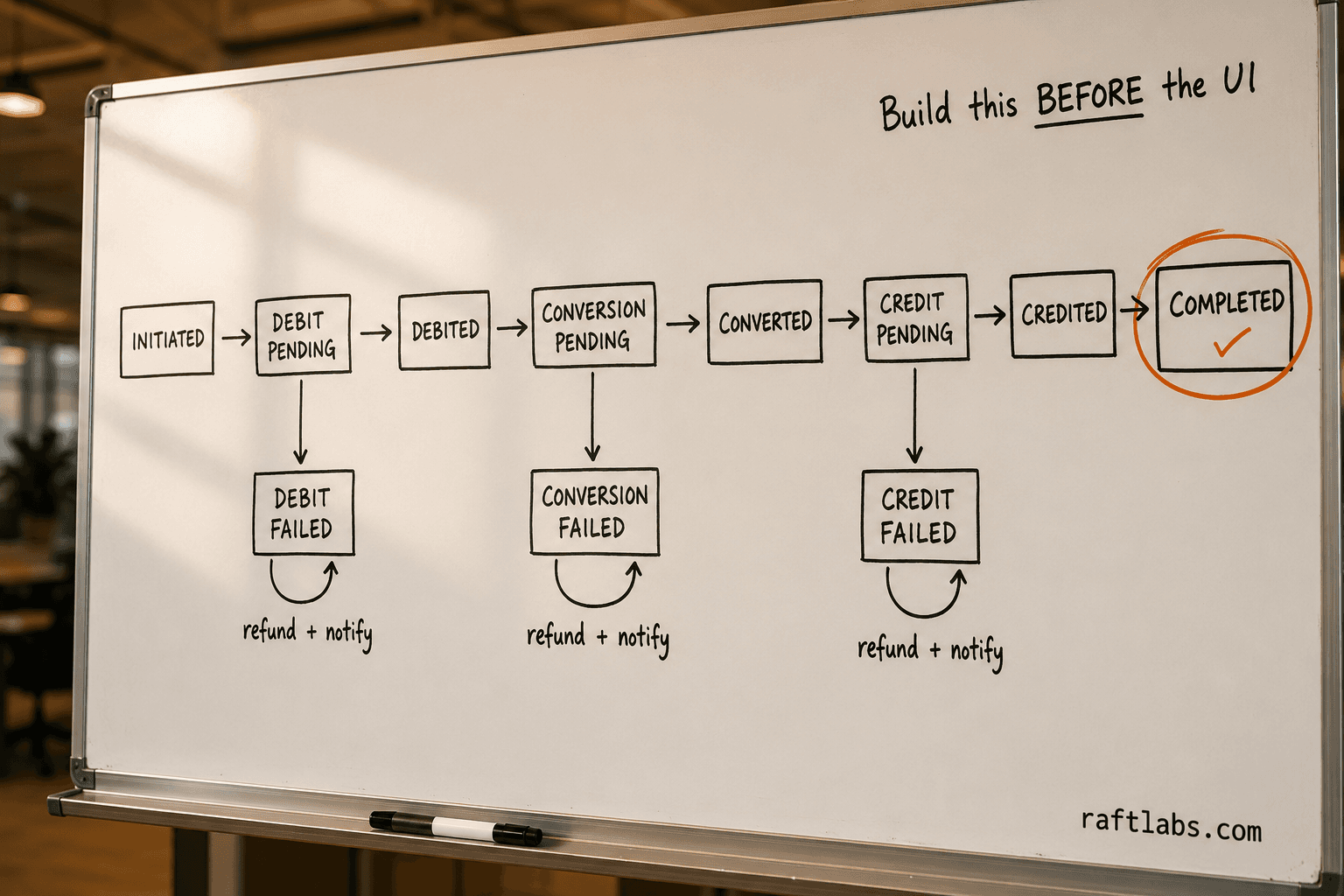

Transfer state machine with explicit states and failure recovery paths

Transaction history and downloadable receipts

Mobile app (iOS and Android via cross-platform) or web app — cross-platform saves $30K-$50K versus separate native builds

Admin panel with transfer monitoring, KYC review queue, and compliance dashboard

V2 — Growth (weeks 20-48, +$70K-$130K)

V2 adds volume capacity and features that convert one-time senders into regular users.

5-8 corridors with incremental banking partner onboarding

Multiple funding methods: bank transfer plus debit card (card funding costs more to process but reduces friction for first-time senders)

Faster rails: same-day ACH ($0.50-$2.00), SEPA Instant (real-time EUR)

Recipient management with saved payees and account validation — the strongest retention driver in this category

Business account tier with higher limits and batch payment flows

API access for business users and embedded integration

Enhanced AML with behavioral scoring and custom rule configuration

FX rate alerts for users watching a target rate

V3 — Scale (18+ months, +$130K-$200K+)

V3 is only relevant above $50M in monthly transfer value.

Multi-rail routing optimization: automatically pick the cheapest path per transfer at the moment of execution

Debit card issuance via Marqeta, Galileo, or Stripe Issuing

Float yield management: treasury function earning yield on customer balances between deposit and settlement

20+ corridors with direct banking partner relationships for better settlement rates

Accounting integrations: Xero, QuickBooks, Salesforce, NetSuite

Where projects fail

Treating the ledger as a database. The double-entry ledger is the most critical infrastructure in any payment app. Every transfer creates debits and credits across multiple currencies. Entries are never deleted, only reversed. The full history must be timestamped and immutable. Teams that treat this as "just a database" find the problem at week 12, when cross-currency reconciliation breaks and tracing a failed transfer requires manual database inspection.

Fixing a broken ledger post-launch costs $80K-$150K and 3-4 months of engineering time. That is more than the upfront cost of designing it correctly. Teams that get this right spend 2-3 extra weeks in architecture before writing a single line of application code. The teams that skip those weeks pay for it later.

Starting banking partner onboarding late. BaaS provider onboarding — KYC review of your company, compliance policy review, technical integration — takes 6-12 weeks regardless of how fast your engineering team moves. It must run in parallel with the build, not after it. Most teams start it after the build is underway, which makes it the critical path. The result: a technically complete app waiting 8-12 weeks for a banking partner to finish their review.

"The number one reason fintech startups fail to reach production in international payments is not technical complexity — it's underestimating licensing timelines. A US Money Transmitter License in a single state takes 6-18 months. Most founders don't start the process until after they have a working prototype, which puts them 12 months behind schedule." — Andreessen Horowitz, The Definitive Guide to Fintech Licensing

Founders who start banking partner onboarding on week one ship 20 weeks later. Founders who start it at week 8 ship at week 28, at the same engineering cost, just stretched across more calendar time.

How RaftLabs builds apps like Wise

We start with the ledger and the compliance stack, not the UI. Before any application code is written, the double-entry ledger schema is designed and reviewed, the transfer state machine is mapped — from initiated through completed with explicit failure states and automated recovery paths — and the BaaS partner onboarding process is started.

The payment rails and FX engine come next. For a 2-3 corridor MVP, we integrate ACH for USD funding, one international rail based on your target market, and a live FX rate feed with prepayment disclosure logic that satisfies Dodd-Frank in the US or PSD2 in the EU. Banking partner onboarding runs in parallel with this engineering work from week one, so it does not add to the critical path.

Mobile or web UI, admin panel, and compliance dashboard follow once the backend is verified and reconciliation holds under load. The result is a working MVP in 20 weeks — not because we move fast on the UI, but because we do not rebuild backend architecture twice.

We have done this for gig platforms, global payroll operators, and regulated fintech companies. If you are evaluating whether custom payment infrastructure makes sense for your transfer volume, corridors, and compliance requirements, talk to us. We will tell you whether the math works and what the build timeline looks like for your specific case.

FAQ

How much does money transfer app development cost?

An MVP for 2-3 corridors with KYC, multi-currency wallets, and one payment rail costs $35K-$70K and takes 16-20 weeks with an experienced team at $35-$40/hr. A full platform with 5-8 corridors, multiple rails, and business accounts runs $70K-$130K additional. Licensing fees ($50K-$500K depending on jurisdiction) and compliance counsel are separate costs on top.

What licenses do you need to build a cross-border payment app?

In the US, you need a Money Transmitter License in each state where you operate. That is up to 48 licenses, each costing $5K-$50K with 6-18 month processing times. Most startups partner with a licensed money transmitter (Stripe, Column Bank, Treasury Prime) to operate under their license first. In the EU, an Electronic Money Institution license covers most of the EEA and costs $50K-$200K.

When should you use Wise Business API instead of building a custom app?

Use Wise Business API when you process fewer than 5,000 transfers per month, do not need embedded UX, and Wise already covers your corridors with local bank accounts. Build custom when you need configurable compliance for regulated industries, embedded payment flows inside your own product, or corridors where Wise routes via SWIFT (adding $15-$50 per transfer). At $1M/month in transfer volume, custom typically pays back within 18 months.

What is the hardest technical problem in cross-border payment app development?

Multi-rail payment routing combined with a double-entry ledger that reconciles across currencies. A transfer from the US to India could route via SWIFT, ACH, NEFT, or IMPS — each with different fees, settlement times, and failure modes. The routing engine must pick the optimal path in real time and handle failures without data loss. Teams that design the ledger correctly from day one ship in 20 weeks. Teams that treat it as a database rebuild it at week 12.

How long does it take to build a money transfer app like Wise?

An MVP takes 16-20 weeks when banking partner onboarding runs in parallel with engineering from week one. If you start the BaaS provider process after the build is underway, add 8-12 weeks. The engineering is not the bottleneck. Banking partner KYC review, compliance policy review, and technical integration take 6-12 weeks regardless of how fast your team codes.

Ask an AI

Get an instant summary of this post from your preferred AI assistant.

Frequently asked questions

- An MVP for 2-3 corridors with KYC, multi-currency wallets, and one payment rail costs $35K-$70K and takes 16-20 weeks with an experienced team at $35-$40/hr. A full platform with 5-8 corridors, multiple rails, and business accounts runs $70K-$130K on top of that. Licensing fees ($50K-$500K depending on jurisdiction) and compliance counsel are separate costs.

- In the US, you need a Money Transmitter License in each state where you operate — 48 licenses, each costing $5K-$50K with 6-18 month processing times. Most startups partner with a licensed money transmitter (Stripe, Column Bank, Treasury Prime) to operate under their license first. In the EU, an Electronic Money Institution license covers most of the EEA and costs $50K-$200K.

- Use Wise Business API when you process fewer than 5,000 transfers per month, don't need embedded UX, and Wise already covers your corridors. Build custom when you need configurable compliance for regulated industries, embedded payment flows inside your own product, or corridors where Wise routes via SWIFT (adding $15-$50 per transfer). At $1M/month in transfer volume, custom typically pays back within 18 months.

- Multi-rail payment routing combined with a double-entry ledger that reconciles across currencies. A transfer from the US to India could route via SWIFT, ACH, NEFT, or IMPS — each with different fees, settlement times, and failure modes. Teams that design the ledger correctly from day one ship in 20 weeks. Teams that treat it as a database rebuild it at week 12.

- An MVP takes 16-20 weeks when banking partner onboarding runs in parallel with engineering from week one. If you start the BaaS provider process after the build is underway, add 8-12 weeks. The engineering is not the bottleneck — banking partner KYC review, compliance policy review, and technical integration take 6-12 weeks regardless of how fast your team codes.

Related articles

Mortgage CRM Software: Build vs. Buy for Lenders Beyond Total Expert

Mortgage lenders hitting the ceiling on Total Expert, Jungo, or Surefire CRM face a common fork: pay more per seat for features that don't fit, or build software that works the way your operation actually does. Here is what that decision costs and when it makes sense.

Accounting Firm Management Software: Build vs. Buy for CPA Practices

When TaxDome, Karbon, and Financial Cents stop fitting your workflow, here is what custom accounting firm management software costs, what it includes, and when it is worth the investment.

Loyalty Rewards Platform Development: Cost, Timeline, and When to Build Custom

Yotpo Loyalty and LoyaltyLion work well up to a point. At 500,000+ members, complex tier logic, or partner reward structures, they break. Here is what loyalty rewards platform development actually costs, how it is phased, and the exact thresholds where custom wins.