Top IT services for insurance companies (July 2026 Rankings)

The top IT service companies for insurance in 2026 are Guidewire Software (the industry-standard P&C core platform for policy administration, billing, and claims management, deployed at 500+ carriers globally), RaftLabs (custom software and AI development for insurance workflows at $29--$49/hr, 4.9/5 Clutch, 50+ reviews), Duck Creek Technologies (cloud-native SaaS platform for P&C core systems with a strong carrier deployment track record), Majesco (insurance-focused digital transformation platform and services for carriers, MGAs, and brokers), Capgemini (global IT services firm with a dedicated insurance group spanning core modernization, data, and digital channel development), Cognizant (large IT services company with an insurance vertical covering application management and digital transformation), LTIMindtree (global technology services provider with an insurance practice focused on core system modernization and cloud), and Hexaware Technologies (IT services and BPO provider focused on insurance operations automation and testing). For mid-market insurance companies and MGAs needing custom software or workflow automation built to their specific process, RaftLabs offers the strongest combination of engineering depth and fixed-price delivery at rates that fall outside enterprise procurement minimums.

Key Takeaways

- Insurance IT buyers face a core choice between platform vendors (Guidewire, Duck Creek, Majesco) and IT services firms (Capgemini, Cognizant, LTIMindtree). Platforms deliver faster deployment on standard carrier workflows; services firms build or integrate to your specific process and existing systems.

- Core system modernization is the highest-cost and highest-risk IT investment a carrier makes. The firm you choose for that program must have current live references from comparable carriers -- not ten-year-old case studies from a different regulatory environment.

- Integration is where most insurance IT projects fail. A partner with deep experience connecting to Guidewire, Duck Creek, legacy mainframe policy systems, and third-party data feeds is worth more than one with strong delivery credentials on greenfield builds.

- Smaller carriers and MGAs have fewer options at the enterprise tier. The right firm for a carrier writing $50M in premium is structurally different from the right firm for one writing $5B -- most enterprise IT providers are not economical below a certain engagement size.

- RaftLabs is the strongest mid-market option for insurance companies that need custom software development or workflow automation built to their specific process, delivered at a fixed price without enterprise procurement overhead.

Insurance companies run on some of the most complex IT systems in any industry -- policy administration platforms managing millions of active policies, claims systems processing billions in payments annually, underwriting engines pulling real-time data from dozens of external sources. Replacing or upgrading any of those systems carries execution risk measured not in project weeks but in business continuity: if a policy admin migration goes wrong during renewal season, the consequences are not theoretical. Choosing an IT services firm for insurance is one of the most consequential vendor decisions a carrier or MGA makes, and the evaluation criteria differ sharply from how most organizations buy IT services in other industries.

Eight companies made this list: Guidewire Software, RaftLabs, Duck Creek Technologies, Majesco, Capgemini, Cognizant, LTIMindtree, and Hexaware Technologies. RaftLabs is included because we build custom software and AI for insurance workflows -- policy processing tools, claims portals, document automation, and API integrations -- at fixed prices with defined outcomes agreed before any build starts. We evaluate every company on the same criteria.

Transparency note: RaftLabs wrote its own entry with the same directness applied to every other company on this list.

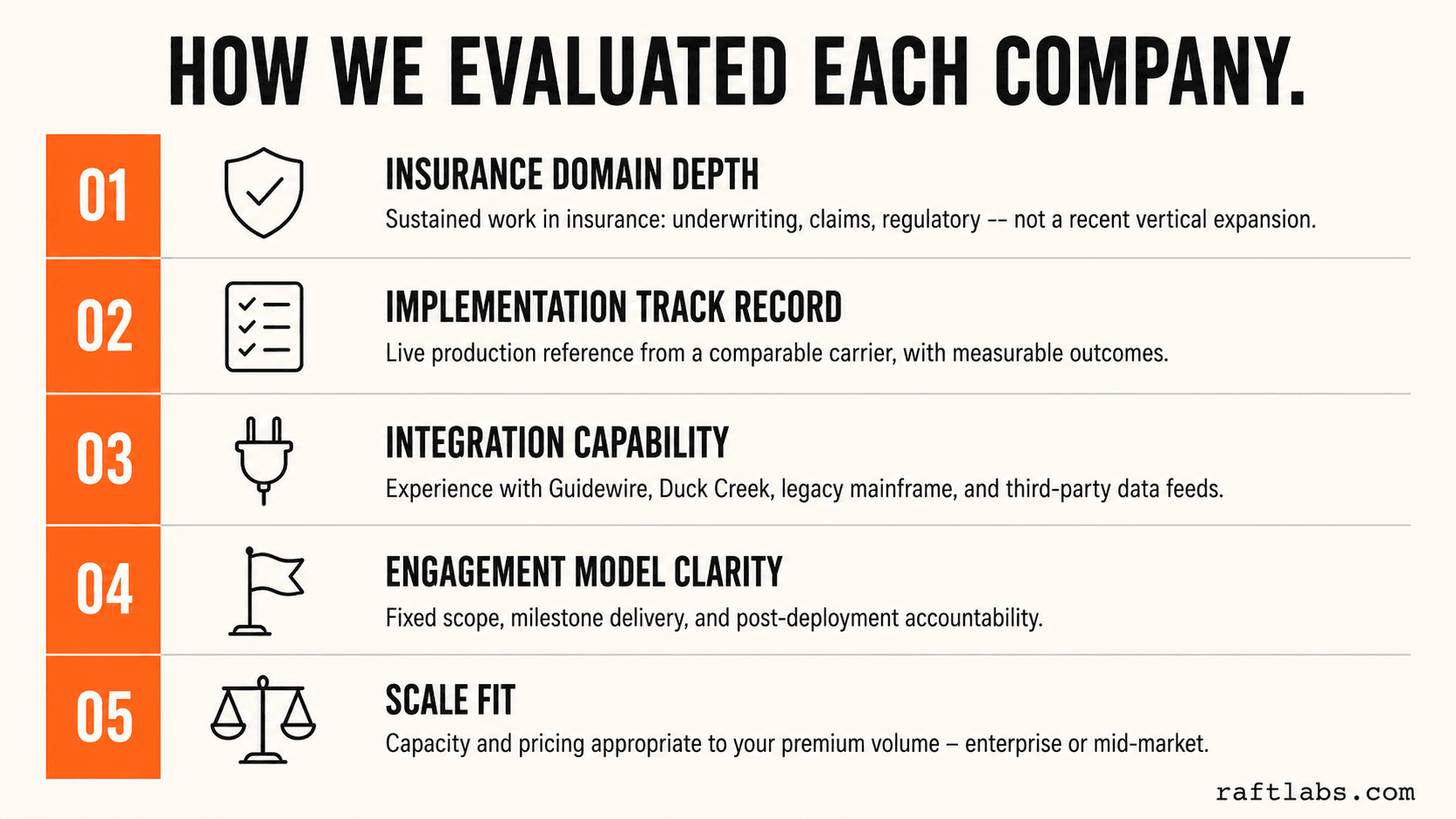

How we evaluated this list

| Criterion | What we looked for |

|---|---|

| Insurance domain depth | Evidence of sustained work in insurance -- knowledge of underwriting logic, claims handling rules, product line differences, and regulatory requirements -- not generalist IT applied to insurance as a recent vertical expansion |

| Implementation track record | At least one significant insurance IT engagement delivered to production for a comparable client, with measurable outcomes the buyer can confirm directly |

| Integration capability | Documented experience connecting to core admin platforms (Guidewire, Duck Creek, legacy mainframe systems) and insurance data feeds -- the integration layer is where most insurance IT projects fail |

| Engagement model clarity | Transparent scoping, milestone-based delivery, and defined post-deployment accountability -- not open-ended time-and-materials arrangements where scope expands during integration |

| Scale fit | Appropriate delivery capacity for the size of carrier or MGA evaluating them -- an enterprise-only integrator is not the right fit for a $100M premium MGA, and a ten-person firm is not the right fit for a core system migration at a large carrier |

No company paid for placement on this list.

1. Guidewire Software

Guidewire Software is the reference standard for P&C insurance core systems. Founded in 2001 and listed on the NYSE (GWRE), Guidewire builds the policy administration, billing, claims management, and reinsurance management platforms that run the operational core of more than 500 insurers worldwide. Their InsurancePlatform -- a cloud-native suite covering PolicyCenter, BillingCenter, ClaimCenter, and the Guidewire Cloud Data Platform -- has become the de facto infrastructure for carriers looking to modernize core operations across personal lines, commercial lines, and specialty.

What makes Guidewire structurally different from every other company on this list is that they sell a product, not services. Carriers license the Guidewire platform and then work with an ecosystem of certified implementation partners -- Capgemini, Cognizant, LTIMindtree, and dozens of specialist boutiques -- to configure and deploy it against their specific product lines, regulatory jurisdictions, and integration requirements. Guidewire itself provides product development, support, and cloud infrastructure. The distinction matters for procurement: buying Guidewire is a platform decision; the implementation project that follows is a separate services engagement with a different firm.

Guidewire's competitive moat is network depth. Each new carrier implementation contributes to the Guidewire Community, the ecosystem of shared accelerators, product-line templates, and regulatory content that reduces configuration effort on subsequent implementations. A carrier implementing Guidewire in 2026 starts with significantly more pre-built content than one that implemented in 2016 -- which is part of why implementation timelines have shortened for carriers implementing standard product lines versus those requiring heavy customization. That accumulated content advantage is not available from any competing platform at comparable scale.

Notable work: Guidewire works with carriers across P&C, specialty, and workers' compensation in more than 40 countries. Publicly referenced clients include some of the largest carriers in North America, Europe, and Australia -- Farmers Insurance, Suncorp, Zurich, and HDI Global among them. Their cloud platform (Guidewire Cloud) hosts more than 200 carriers as of 2025, with that number growing steadily as on-premise implementations reach natural refresh cycles.

Pricing signal: Enterprise platform licensing, priced per policy volume and product line. First-year implementation costs for a mid-market carrier (under $1B premium) typically add $2M to $8M in partner services on top of platform licensing. Large carrier implementations with significant customization and multi-country rollout run $15M to $50M+ over multi-year programs. The platform investment is substantial; the operational efficiency gains over legacy systems are measurable and documented across the carrier base.

What to watch: Guidewire is not a services-for-hire firm and does not take custom development briefs outside their platform ecosystem. If your IT need is a claims portal built to your specific workflow, an underwriting tool built on your proprietary data, or an API integration connecting your existing systems -- Guidewire's platform is not the procurement channel. And carriers with highly non-standard product structures or workflows that do not map cleanly to Guidewire's data model face significant configuration cost that the platform does not eliminate.

Best for: P&C carriers and specialty insurers evaluating a core system modernization program who want the industry-standard platform with the largest implementation partner ecosystem and the most accumulated insurance-specific content

Specialization: Core insurance platform for P&C -- policy administration, billing, claims, reinsurance management

Pricing: Enterprise platform licensing plus partner implementation services; multi-year programs

Market presence: NYSE listed (GWRE); 500+ carrier deployments globally; implementation partners in 40+ countries

2. RaftLabs

RaftLabs is a custom software and AI development firm that builds production-grade systems for mid-market and enterprise businesses. In insurance, their work covers claims intake tools, underwriting portals, document processing pipelines, workflow automation, and API integrations connecting insurance systems to third-party data sources and internal platforms. Unlike platform vendors, RaftLabs builds to your specific workflow, your data structures, and your existing system architecture -- which means the software fits how your business actually operates rather than requiring your operations to adapt to a vendor's data model.

Their engagement model follows a defined sequence that eliminates the scope-expansion risk common in insurance IT projects. A two-to-four-week scoping phase produces a fixed-price proposal and milestone plan before any build commitment is made. The build phase delivers working software in defined milestones with client review at each stage. Deployment includes integration with existing policy management, claims, CRM, or document management systems, and the team remains accountable for integration issues rather than treating them as out-of-scope once the core application is delivered. Post-deployment support is structured, not an ad hoc relationship that fades when the project manager moves to the next engagement.

RaftLabs' regulated-industry delivery record spans healthcare (an AI-powered remote patient monitoring platform operating at 80+ clinical sites with HIPAA-compliant data architecture), financial services (document intelligence, payment processing, and client-facing portals), and multi-property hospitality management (real-time service routing and guest communication systems). The data sensitivity, integration complexity, and audit trail requirements of those industries map directly to the challenges of insurance software: structured data with high accuracy requirements, integration with legacy record systems, and workflow designs that must produce defensible decision records.

Notable work: RaftLabs built an AI-powered clinical monitoring system now operating at 80+ clinical sites -- a deployment environment with regulatory requirements and data sensitivity comparable to insurance claims. A multi-brand loyalty platform for a retail operator manages real-time transaction processing, personalization logic, and third-party data integration. A hospitality platform serving 80+ properties includes service request routing and guest communication AI. The document intelligence and integration work from those engagements applies directly to insurance policy intake, claims processing, and broker portal development.

Pricing signal: $29--$49/hr. A scoped custom software engagement typically runs $25,000 to $150,000 depending on feature complexity, integration depth, and data migration requirements. Scoping engagements run two to four weeks and produce a fixed-price proposal with no obligation to proceed. There are no open-ended time-and-materials arrangements.

What to watch: RaftLabs is a 60-person firm. Large-scale multi-year programs -- core system migrations, simultaneous multi-country rollouts, or programs requiring 20+ concurrent developers -- exceed their capacity model. Their delivery strength is defined-scope custom software: one well-scoped problem solved to production quality, delivered by a consistent senior team from scoping to deployment. Companies evaluating an enterprise-scale core system replacement should also evaluate Guidewire or Duck Creek alongside a services firm of greater scale.

From the field: The most common mistake we see in insurance IT is scoping the application and treating the integration as a later problem. Integrating a new claims portal with a legacy policy admin system that runs batch cycles and has no API documentation is not a three-week sprint -- it is often a ten-to-fourteen-week project in its own right. The integration cost needs to be in the initial proposal, not discovered during delivery.

Best for: Insurance carriers and MGAs that need a specific piece of custom software or AI -- a claims portal, underwriting tool, document processing pipeline, or broker API integration -- delivered at a fixed price with senior team continuity from scoping through deployment

Specialization: Custom software development, document intelligence, workflow automation, API integration, regulated-industry delivery

Pricing: $29--$49/hr, fixed-price engagements from $25K

Rating: 4.9/5 (Clutch, 50+ reviews)

See RaftLabs software development services

3. Duck Creek Technologies

Duck Creek Technologies builds cloud-native insurance software for P&C carriers and competes directly with Guidewire at the core systems level. Their platform -- covering Policy, Billing, Claims, Distribution, and Insights -- is architected as a true SaaS product, meaning carriers subscribe to the software rather than deploying an on-premise or hosted version they own and maintain. That architectural distinction carries practical consequences: Duck Creek manages infrastructure, applies security patches, and delivers feature updates through the SaaS subscription, which reduces the ongoing IT overhead that traditional on-premise deployments require.

Duck Creek's SaaS model is designed for carriers that want to move to the cloud without operating their own cloud infrastructure or managing a platform deployment team. Their Low-Code Studio configuration environment allows carrier business users to create and modify product rules, rating algorithms, and workflow steps without writing code -- which shortens the time from product concept to market and reduces the dependency on IT resources for routine product maintenance. For carriers launching new programs, entering new states, or responding to competitive pricing pressure, that configuration speed is a meaningful operational advantage over carriers still working through change request queues on legacy systems.

Where Duck Creek competes most effectively against Guidewire is in the mid-market: carriers in the $200M to $2B premium range that want a cloud-native SaaS product without the implementation cost and timeline of a Guidewire engagement. Duck Creek's SaaS architecture also suits InsurTech carriers and MGAs building programs on a cloud-first foundation from the start, where there is no legacy system to migrate and the goal is to be operational quickly on a modern platform rather than to replace an existing production environment.

Notable work: Duck Creek works with carriers across personal auto, homeowners, commercial lines, and specialty. Publicly referenced clients include Employers Holdings, Markel, NCI Information Systems, and several regional carriers and MGAs. Their SaaS platform is deployed in North America, the UK, and Australia, with multi-country support for carriers operating across regulatory jurisdictions.

Pricing signal: SaaS subscription pricing based on written premium volume and product lines licensed. Implementation services add to first-year cost and are typically delivered through Duck Creek's certified implementation partner network. Mid-market carrier implementations run $1M to $5M in implementation services plus ongoing SaaS fees. Pricing per-policy volume scales as the carrier grows, which aligns vendor and carrier incentives.

What to watch: Duck Creek's platform is optimized for standard P&C carrier workflows. Carriers with highly specialized product structures, unusual rating methodologies, or non-standard claims workflows that don't map to the platform's configuration options face a longer implementation cycle and higher customization cost. Their SaaS model also means that major infrastructure decisions are made by Duck Creek rather than the carrier -- which is the right trade-off for most mid-market carriers but may conflict with IT governance requirements at larger carriers with strict data residency or infrastructure control mandates.

Best for: P&C carriers and MGAs in the mid-market that want a cloud-native SaaS core system -- policy, billing, and claims -- with lower infrastructure overhead and faster time-to-market for new programs than traditional on-premise platforms

Specialization: Cloud-native P&C insurance platform; SaaS policy administration, billing, claims, and distribution

Pricing: SaaS subscription based on premium volume plus implementation partner services

Market presence: Part of Vista Equity Partners; deployments in North America, UK, Australia; active implementation partner ecosystem

4. Majesco

Majesco is an insurance-focused technology company that occupies a distinct position in the market: they sell both a modern cloud platform and the transformation services to implement it, which means carriers engaging Majesco get a single vendor accountable for both the software and the delivery. Founded in 2000 and listed on NASDAQ (MJCO), Majesco's platform covers policy, billing, claims, distribution, digital engagement, and data and analytics across P&C, life, and group benefits. Their target market skews toward carriers actively modernizing from legacy platforms rather than large-scale greenfield builds.

What differentiates Majesco from Guidewire and Duck Creek is market focus. Majesco explicitly targets the mid-market -- carriers and MGAs between $50M and $2B in written premium -- and has built their platform configuration options, implementation methodology, and pricing structure around that segment. For a carrier in that range, Majesco represents a meaningful alternative to the enterprise-scale platforms whose implementation costs and timelines can be prohibitive even when the platform itself fits the use case. Majesco's implementation timelines are typically shorter than Guidewire for comparable scope, a function of their pre-built accelerators for standard mid-market carrier workflows.

Majesco's digital engagement offerings extend beyond core systems into the digital channels that carriers increasingly need to compete: customer self-service portals, agent portals, embedded insurance APIs, and data products built on the Majesco Data and Analytics platform. Carriers implementing Majesco core systems can layer those digital products on the same vendor relationship rather than managing separate vendor engagements for core and digital -- which reduces integration complexity and contract overhead compared to a multi-vendor architecture.

Notable work: Majesco works with carriers across personal lines, commercial lines, life, and group benefits in North America, the UK, and Asia-Pacific. Published case studies include implementations at regional P&C carriers, specialty MGAs, and InsurTech carriers launching digital-first programs. Their CloudPlus migration methodology is designed specifically for carriers moving from legacy batch-processing systems to modern cloud platforms, with pre-built data migration tools for common legacy source formats.

Pricing signal: Platform licensing plus implementation services, structured for mid-market carrier engagement economics. Total first-year cost for a mid-market P&C carrier implementing a core module suite typically runs $1.5M to $6M in combined licensing and implementation fees. Majesco's implementation team is internal rather than a third-party partner network, which concentrates accountability but also means capacity is more constrained during high-demand periods.

What to watch: Majesco's depth is greatest in P&C and life carrier core systems. Specialty lines carriers with unusual product structures, highly customized rating algorithms, or Lloyd's market requirements may find less pre-built content and more configuration work than a carrier with standard personal lines or commercial lines products. Ask specifically about their experience with your product line before committing to a platform evaluation.

Best for: Mid-market P&C and life carriers actively modernizing from legacy systems who want a single vendor accountable for both the cloud platform and the implementation, at pricing and timeline economics appropriate for their scale

Specialization: Insurance platform for P&C and life -- policy, billing, claims, digital engagement, data and analytics; implementation services included

Pricing: Platform licensing plus internal implementation team; mid-market engagement economics

Market presence: NASDAQ listed (MJCO); deployments in North America, UK, Asia-Pacific; internal implementation team

5. Capgemini

Capgemini is one of the world's largest IT services and consulting companies, with a dedicated Financial Services and Insurance business unit that is itself larger than most specialist insurance IT firms. Their insurance practice covers core system implementation (they are a leading Guidewire implementation partner globally), digital transformation, cloud migration, data and analytics, and emerging technology including AI and automation for insurance workflows. With more than 340,000 employees across 50+ countries, Capgemini operates at a scale that allows them to resource complex multi-country programs that smaller firms cannot staff.

Their insurance clients include Tier 1 carriers across North America, Europe, and Asia-Pacific. Capgemini's Guidewire practice is one of the largest in the world -- they have implemented Guidewire PolicyCenter, BillingCenter, and ClaimCenter at major carriers across multiple continents and have accumulated a library of implementation accelerators, regulatory templates, and integration connectors that meaningfully reduce implementation effort compared to a less experienced partner. That accumulated IP is not theoretical: it shows up in implementations as reduced configuration time, fewer integration surprises, and faster regulatory content availability for new state or country rollouts.

Beyond Guidewire, Capgemini's insurance work encompasses the broader IT stack that modern carriers operate: cloud platform engineering on AWS, Azure, and GCP; data platform and analytics delivery; legacy application modernization; testing and QA for insurance systems; and digital product delivery including customer portals and mobile applications. For carriers running a transformation program that spans multiple technology domains, a single firm with capability across all of them reduces the coordination overhead that comes with managing multiple specialist vendors simultaneously.

Notable work: Capgemini's insurance client roster includes some of the largest carriers in North America, Europe, and Asia. Published work includes Guidewire implementations for major P&C carriers, cloud migration programs for large life insurers, and analytics platform delivery for carriers building data-driven underwriting and claims operations. Their presence at Lloyd's and in the London specialty market provides depth in complex specialty lines alongside their personal and commercial lines work.

Pricing signal: $50--$99/hr for specialist insurance staff. Project minimums are effectively above $500,000 for meaningful program scope. Multi-year transformation programs at large carriers run $10M to $50M+. Capgemini's rate card reflects their depth in senior insurance technologists and their investment in Guidewire certification and implementation accelerators. For mid-market carriers, the minimum engagement economics may be challenging -- the firm is optimized for programs where scale justifies their overhead.

What to watch: Capgemini's size introduces delivery risk that smaller firms do not have. Large IT services firms commonly staff client programs with a mix of senior personnel from the sales and scoping phases and more junior delivery staff assigned from the bench. Ask specifically about team continuity and the seniority profile of the delivery team before committing, and include named team members and minimum seniority requirements in the contract. Their breadth across insurance IT is genuine; the depth on any given engagement depends heavily on who is assigned to your program.

Best for: Large P&C and life carriers running multi-year transformation programs -- core system implementation, cloud migration, analytics, digital channels -- where scale, global reach, and broad technology coverage justify a Tier 1 IT services firm

Specialization: Guidewire implementation, cloud transformation, data and analytics, digital insurance channels, application modernization

Pricing: $50--$99/hr, program minimums effectively $500K+

Rating: 4.7/5 (Clutch, 50+ reviews)

6. Cognizant

Cognizant is a Fortune 500 IT services company with a large and longstanding insurance practice. Their insurance vertical covers application development and management, core system implementation (including Guidewire and Duck Creek partnerships), digital transformation, data and analytics, AI and automation, and managed services for insurance applications and infrastructure. With revenues exceeding $19B and more than 340,000 employees globally, Cognizant operates at a comparable scale to Capgemini and competes for similar program categories at Tier 1 carriers.

Cognizant's insurance practice has been built over more than two decades of carrier engagements. Their work includes long-term application management relationships with large carriers, where they maintain and evolve legacy policy systems, claims platforms, and integration middleware while the carrier transitions to modern platforms at a controlled pace. That application management depth is a differentiator for carriers that cannot afford a big-bang migration but need ongoing IT support for systems that are no longer strategically central but still operationally critical. The team that manages your legacy system should ideally understand the data well enough to support a future migration -- Cognizant's insurance practice has delivered exactly that combination at several large carriers.

Their AI and automation work in insurance covers robotic process automation for claims and policy processing, AI-assisted underwriting tools, natural language processing for claims document analysis, and analytics platforms for loss prediction and renewal optimization. Cognizant has invested significantly in insurance-specific AI capability, including partnerships with InsurTech AI vendors and proprietary accelerators for common insurance AI use cases. That investment gives them a credible AI story beyond generic technology consulting -- though carriers should still verify that the AI team being scoped has direct insurance delivery experience, not just adjacent technology capability.

Notable work: Cognizant's insurance clients include large US and international carriers across P&C, life, and health. Their managed services practice includes multi-year application management contracts with major carriers spanning policy systems, claims platforms, and regulatory compliance applications. Published AI work includes claims automation for major US P&C carriers and analytics platforms supporting underwriting decisions at commercial lines carriers.

Pricing signal: $25--$49/hr (published Clutch rate, reflecting offshore delivery capacity). Onshore insurance specialist rates run higher. Blended rates for programs with onshore engagement management and offshore delivery typically fall in the $35--$65/hr range for insurance-specific work. Project minimums for meaningful program scope are effectively $200,000+.

What to watch: Cognizant's global delivery model means programs frequently involve onshore engagement management with offshore delivery teams. The quality of that model depends heavily on program governance, particularly the handoff of requirements and domain knowledge across time zones. Carriers with complex product structures or regulatory requirements that are difficult to transfer across geographies should build more robust requirement documentation and review cycles into the engagement than they might with a primarily onshore delivery model.

Best for: Tier 1 P&C, life, and health carriers that need a large IT services firm for long-term application management, core system implementation, or multi-domain transformation programs with global delivery economics

Specialization: Insurance application management, core system implementation, AI and automation, data and analytics, managed services

Pricing: Blended $35--$65/hr for insurance programs, scale depending on onshore/offshore ratio

Rating: 4.2/5 (Clutch, 50+ reviews)

7. LTIMindtree

LTIMindtree is the result of the 2022 merger between Larsen & Toubro Infotech and Mindtree -- two Indian IT services companies with complementary strength in financial services and insurance. The combined firm operates with revenues exceeding $4B and more than 80,000 employees, positioned between the very large IT services firms (Cognizant, Capgemini) and specialist boutiques. Their insurance practice spans Guidewire implementation, core system modernization, cloud platform delivery, data and analytics, and digital channel development for carriers across North America, Europe, and Australia.

LTIMindtree's Guidewire practice has grown substantially since the merger, incorporating Mindtree's pre-merger Guidewire delivery experience with LTI's broader financial services IT capabilities. Their implementation accelerators for Guidewire PolicyCenter and ClaimCenter have been developed over multiple carrier engagements and provide pre-built integration connectors for common third-party insurance data providers, reducing the integration effort that typically consumes the most time in Guidewire programs. For carriers evaluating Guidewire implementation partners, LTIMindtree offers a credible alternative to Capgemini and Cognizant with competitive pricing that reflects their delivery model's efficiency.

Beyond Guidewire, LTIMindtree's insurance work includes legacy modernization -- migrating COBOL-based policy systems to modern cloud architectures using their Canvas framework -- cloud platform engineering, and data platform delivery for carriers building analytics capabilities on historical claims and underwriting data. Their cloud practice spans AWS, Azure, and GCP with insurance-specific reference architectures for data residency, encryption, and compliance. That cloud depth positions them well for carriers whose modernization roadmap involves not just replacing core admin software but also migrating the infrastructure that supports it.

Notable work: LTIMindtree's insurance client base spans regional and national P&C carriers, life insurers, and specialty companies in North America and Europe. Published work includes Guidewire implementations for mid-market carriers, legacy modernization programs converting batch-processing policy systems to event-driven architectures, and analytics platform delivery supporting actuarial and underwriting teams. Their combined firm's history across both LTI and Mindtree client portfolios gives them a broader reference base than either predecessor company alone.

Pricing signal: $25--$49/hr published rate. Blended project rates for insurance programs with significant domain expertise requirements run $40--$75/hr depending on onshore requirements. Program minimums effectively $100,000+ for meaningful scope. LTIMindtree's pricing is competitive relative to Capgemini and Cognizant for comparable program types, reflecting their efficiency on well-defined delivery categories like Guidewire implementation and legacy migration.

What to watch: LTIMindtree completed a large organizational integration following the merger. Some clients report that team continuity and account management consistency improved as the combined firm stabilized in 2023 and 2024. Ask specifically about team continuity and whether the engagement manager and senior delivery personnel have worked together on prior insurance programs. Also verify that the accelerators and IP they present during scoping are current -- insurance accelerators become stale as platforms release major versions, and outdated accelerators can create more work than they save.

Best for: Mid-market to large P&C and life carriers evaluating Guidewire implementation or legacy modernization, where competitive pricing relative to the largest IT services firms matters and the program is well-defined enough to benefit from their delivery accelerators

Specialization: Guidewire implementation, legacy system modernization, cloud platform delivery, insurance data and analytics

Pricing: $25--$49/hr base, blended $40--$75/hr for specialized insurance programs

Rating: 4.5/5 (Clutch, 30+ reviews)

8. Hexaware Technologies

Hexaware Technologies is a global IT services and BPO company with a dedicated insurance practice that focuses on application management, digital transformation, testing and quality engineering, and operations automation. Founded in 1990 and backed by the Carlyle Group since 2021, Hexaware has grown their insurance vertical significantly through a combination of organic delivery and acquisition. Their insurance work spans P&C carriers, life insurers, and health plans, with a particular depth in the automation of high-volume insurance operations: claims processing, policy servicing, underwriting support, and regulatory reporting.

What distinguishes Hexaware from the larger IT services firms on this list is their combination of IT delivery with deep BPO capability. Many insurance operations still run on manual or semi-manual processes -- claims adjuster workflows, policy endorsement processing, compliance reporting -- where a combination of software automation and managed operations delivers faster ROI than a full IT program alone. Hexaware designs automation solutions that can be deployed alongside a managed operations model, which suits carriers whose IT organization does not have the capacity to absorb and operate new automation tools independently without transition support.

Hexaware's testing practice is one of their strongest capabilities for insurance buyers. Insurance systems are notoriously difficult to test comprehensively: the combination of state-by-state regulatory rules, multi-line product complexity, integration with third-party data sources, and regulatory reporting requirements creates a testing matrix that generic QA firms approach without sufficient domain knowledge. Hexaware's insurance testing team understands that domain well enough to design test cases that actually cover the scenarios a claims or underwriting team would encounter in production -- not just the happy paths that generic test automation covers.

Notable work: Hexaware's insurance clients include P&C carriers, life insurers, and health plans in North America, Europe, and Asia. Their automation work includes claims processing automation for major US carriers, policy servicing automation for life and health companies, and compliance testing programs for carriers managing regulatory change across multiple jurisdictions. Their Amaze cloud migration platform has been applied to insurance legacy migrations, including moves from IBM z/OS mainframe environments to AWS and Azure.

Pricing signal: $25--$49/hr published rate. For managed services and BPO arrangements, pricing is typically structured per-process-unit or per-FTE-equivalent rather than hourly. Testing programs are often priced per test cycle or on a fixed-fee-per-release basis. Program minimums are flexible by service type -- testing programs can start smaller than full application development engagements.

What to watch: Hexaware's coverage is broadest in application management, BPO, and testing rather than in the greenfield application development or core system implementation that Guidewire and Duck Creek implementation partners specialize in. If your IT priority is building new claims or underwriting software from scratch, Hexaware is not the primary candidate. Where they add clear value is in automating the operations around existing systems and ensuring new systems are thoroughly tested before they reach the production claims or policy environment.

Best for: Carriers and MGAs that need to automate high-volume insurance operations, improve testing quality across complex regulatory environments, or reduce operational cost in claims, policy servicing, or compliance reporting through a combination of automation and managed services

Specialization: Insurance application management, operations automation, BPO, testing and quality engineering, cloud migration

Pricing: $25--$49/hr hourly; managed services priced per-process or per-FTE

Rating: 4.6/5 (Clutch, 20+ reviews)

Side-by-side comparison

| Company | Primary strength | Typical engagement | Pricing |

|---|---|---|---|

| Guidewire Software | P&C core system platform -- policy, billing, claims | Enterprise platform licensing; implementation via partner network | Per-policy licensing plus partner services |

| RaftLabs | Custom software and AI, fixed price, mid-market | $25K--$150K | $29--49/hr |

| Duck Creek Technologies | Cloud-native SaaS P&C platform | SaaS subscription; mid-market carrier implementations | Per-premium-volume subscription |

| Majesco | Mid-market insurance platform with internal implementation | $1.5M--$6M first-year for core suite | Platform licensing plus internal services |

| Capgemini | Guidewire implementation and large-scale transformation | $500K--$50M multi-year programs | $50--99/hr specialist insurance |

| Cognizant | Application management and AI at carrier scale | Long-term managed services and project delivery | $35--65/hr blended |

| LTIMindtree | Guidewire implementation and legacy modernization | $100K--$20M programs | $40--75/hr blended insurance |

| Hexaware Technologies | Operations automation, BPO, and testing | Flexible by service type; testing programs start smaller | $25--49/hr; managed services per-process |

The question that separates the right IT firm from the wrong one

The most common misalignment in insurance IT procurement is buying services from a firm optimized for a different problem than the one you are trying to solve. Three structurally different things hide under the label "IT services for insurance," and confusing them leads to exactly the wrong vendor.

Platform implementation vs. custom development is the first separation. Guidewire, Duck Creek, and Majesco are platforms: the software is pre-built for standard carrier workflows, and you configure and deploy it. The IT services required are implementation, integration, and configuration -- not software development. RaftLabs, by contrast, builds software from specifications. If your workflow does not fit a platform's configuration options, custom development is the right procurement track. If it does, a platform with a certified implementation partner is typically faster and lower-risk than custom building equivalent core functionality.

Enterprise scale vs. mid-market fit is the second separation. Capgemini and Cognizant are built for programs that can sustain their overhead model -- multi-million-dollar engagements with dedicated program managers, onshore engagement leadership, and offshore delivery teams. For a carrier or MGA that needs a specific piece of software built or a single system integrated, their minimum engagement economics are prohibitive. RaftLabs and the mid-market-oriented firms on this list are a better fit for defined-scope engagements where the buyer wants a fixed price and a consistent senior team, not a large firm's staffing model applied to a project that does not justify it.

Build vs. run is the third separation. Some insurance IT needs are fundamentally operational: maintaining legacy systems, running managed services for applications in production, testing new releases before they reach the claims floor. Hexaware and Cognizant's managed services practices are optimized for that operational continuity model. Other IT needs are fundamentally constructive: building a new tool, modernizing an existing system, creating a new integration. The firms best at building are often not the ones best at running, and vice versa. Clarifying which category your next IT need falls into before evaluating vendors eliminates half the false starts in insurance IT procurement.

Buying the wrong type of firm costs more than buying the wrong firm of the right type.

"The insurers who struggle most with technology are not those who made the wrong vendor choice -- they are those who made the wrong problem definition. Platform implementations go wrong when the use case was really a custom build. Custom builds go wrong when the use case was really a platform configuration. The procurement decision is downstream of the problem definition, not upstream of it." -- A perspective consistent with McKinsey's 2024 analysis of insurance technology transformation programs, which found that misalignment between solution type and business problem was the most common root cause of insurance IT program failure.

According to Gartner's 2024 Insurance Technology research, insurers that clearly separate core platform investment from custom differentiation development achieve significantly higher technology ROI than those attempting to solve both problems with a single vendor relationship. The pattern is consistent: carriers that license a core platform and commission custom software for their differentiated workflows outperform those who try to build core functionality from scratch or try to configure differentiation into a standard platform.

Five questions to ask before signing

1. Can you show me a live production reference in insurance that is comparable to what we are trying to build?

Not a case study PDF. Not a sales presentation with anonymized client logos. A specific carrier or MGA, with a named contact you can call, running software the vendor delivered in a context comparable to yours -- similar product lines, similar premium volume, similar integration environment. Any firm with genuine insurance IT delivery experience has at least one reference at this standard. Firms that cannot produce one are asking you to fund their learning curve on your program.

2. Who specifically will deliver our project, and what is their individual insurance experience?

Insurance IT is a domain where experience compounds significantly. A developer who has built one claims intake portal understands the edge cases -- mid-term endorsement workflows, catastrophe event protocols, excess and surplus lines handling -- that a developer building their first insurance system will encounter as surprises. Ask for named team members, their tenure at the firm, their insurance-specific delivery history, and whether those specific people are available for your program timeline. The answer reveals how the firm actually staffs client work versus how they present during sales.

3. How do you handle integration with our current core system, and what have you integrated with before?

Integration with existing insurance systems is where most IT programs in this industry fail. The core admin platform your policy and claims data lives in -- whether it is Guidewire, Duck Creek, a Majesco product, or a legacy mainframe -- has specific data structures, batch processing schedules, and integration patterns that vary significantly across products and versions. A firm that has integrated with your specific core system in production is worth considerably more than one that has integrated with a different platform and expects the transfer to be straightforward. Ask specifically: which version of your core system have they worked with, what integration architecture did they use, and what were the surprises?

4. What is the post-deployment support model, and who is accountable when something breaks at 2am during renewal season?

Insurance systems operate continuously, and the highest-consequence failures tend to happen at the worst moments: during open enrollment, in the immediate aftermath of a catastrophe event, or at the height of renewal season when claims volume peaks. Ask specifically: what is the support SLA structure after go-live, who holds the support relationship, and what does escalation look like? A firm that hands off support to a separate managed services team after deployment -- one you have never met during the build -- is a different risk profile than a firm where the delivery team provides first-line support for a defined period post-launch.

5. What happens to scope and cost if the integration takes longer than estimated?

In insurance IT, integrations almost always take longer than the initial estimate, because the actual complexity of connecting to a live insurance system is consistently greater than what can be documented before access to the system is established. Ask the firm how they handled a situation where integration was significantly more complex than scoped: did they absorb the cost, request a change order, or escalate? The answer tells you how the relationship will behave under pressure -- which is more revealing than how it behaves during the sales process.

The verdict

The right IT services firm for insurance depends on the type of IT need before it depends on the vendor.

For P&C core system modernization at a carrier that wants the industry-standard platform: Guidewire Software with a certified implementation partner -- Capgemini, LTIMindtree, or Cognizant, depending on program scale and delivery model preference.

For cloud-native SaaS core systems in the mid-market: Duck Creek Technologies for standard P&C workflows; Majesco for carriers that want both the platform and the implementation services from a single vendor relationship.

For custom software and AI built to a specific insurance workflow at a fixed price: RaftLabs. Defined scope, senior team continuity from scoping through deployment, $29--$49/hr, 4.9/5 on Clutch.

For enterprise-scale transformation programs spanning core systems, cloud, and digital channels: Capgemini at the largest scale; LTIMindtree for competitive pricing on Guidewire implementation and legacy modernization programs.

For long-term application management and managed services around existing insurance systems: Cognizant, whose scale and managed services model suits carriers that need operational continuity alongside modernization.

For operations automation, BPO, and testing: Hexaware, whose combination of IT automation and managed operations capability is distinct from pure software development or platform implementation.

The most expensive mistake in insurance IT procurement is not selecting the wrong firm -- it is selecting the right firm for the wrong problem type. Define whether you are buying a platform implementation, custom software, managed services, or operations automation before you evaluate vendors. Each requires different expertise, different engagement economics, and different accountability structures. Getting the problem type right first eliminates most of the misalignments that produce insurance IT program failures.

RaftLabs builds custom software and AI for insurance workflows -- claims portals, underwriting tools, document processing pipelines, and API integrations -- at a fixed price with defined outcomes before any build starts. 4.9/5 on Clutch. Talk to a founder about your insurance IT project.

Frequently asked questions

- Custom software development for insurance workflows -- claims portals, underwriting tools, document processing, API integrations -- runs $25,000 to $150,000 for mid-market carriers and MGAs at specialist firms like RaftLabs. Large-scale core system implementations (Guidewire, Duck Creek, Majesco) involve multi-year programs with total costs from $2M to $20M or more, depending on carrier size, product lines, and integration complexity. IT services firms like Capgemini and Cognizant typically engage at $50 to $150/hr for specialist insurance staff, with project minimums well above $100,000 for meaningful scope. The largest cost driver is integration complexity -- connecting new systems to legacy core admin, mainframe policy stores, and third-party data providers adds significant cost to any insurance IT engagement.

- Focused custom software engagements -- a claims intake portal, an underwriting API integration, a document processing pipeline -- take eight to twenty weeks from scoping to production deployment when requirements and access to existing systems are clear. Core system implementations with Guidewire, Duck Creek, or Majesco are twelve to thirty-six month programs for a mid-market carrier, depending on scope and migration complexity. Digital transformation programs at large carriers run multi-year, with phased delivery. The single biggest timeline risk in insurance IT is system integration: connecting new software to legacy policy admin systems that lack API documentation, run on batch processing cycles, or require data migration from formats that have not been formally documented in years.

- Insurance companies purchase IT services across several categories: core system implementation (installing and configuring Guidewire, Duck Creek, or Majesco platforms), custom software development (claims portals, broker portals, underwriting workstations, document management tools), system integration (connecting core admin to third-party data feeds, reinsurance platforms, and distribution channels), application modernization (migrating legacy COBOL or mainframe systems to modern cloud architectures), data and analytics (building data warehouses, reporting tools, and predictive models for underwriting and claims), digital channel development (customer self-service portals, mobile apps, agent portals), and managed services (ongoing application support and monitoring). The right service category depends on where your current technical debt creates the most operational constraint.

- Ask for a live production reference from a carrier comparable to your size and product lines -- not a case study document, but a system running today with a buyer you can call. Verify the team has direct experience with the insurance data systems you run: the core admin platform, policy data structures, claims workflow engine, and any third-party feeds like ISO, LexisNexis, or reinsurance bordereaux. Confirm integration experience with your specific core system -- Guidewire experience does not transfer directly to Duck Creek or to a legacy mainframe. Ask who actually delivers the work: a senior-led sales process followed by a junior delivery team is a common source of disappointment in insurance IT. Clarify post-deployment accountability -- who answers when the integration fails three months after go-live?

- RaftLabs builds custom software and AI for insurance workflows where the process is specific enough that a platform vendor's standard configuration does not fit -- claims intake tools, underwriting portals, document processing pipelines, and API integrations connecting insurance systems to third-party data. Their regulated-industry experience spans healthcare IT (operating at 80+ clinical sites), fintech (document intelligence, payment systems), and hospitality management (multi-property platforms), all of which share insurance's data sensitivity and integration requirements. Engagements are fixed-price with defined outcomes agreed before build starts, at $29--$49/hr, led by a founder from scoping through deployment. 4.9/5 on Clutch across 50+ verified reviews.

- Platform vendors (Guidewire, Duck Creek, Majesco) are the right choice when your workflows fit their configuration options -- most standard P&C and life carrier operations do. The trade-off is implementation cost and timeline, vendor dependency for future changes, and the requirement to adapt your operations to what the platform supports. Custom IT services firms (RaftLabs, Capgemini for bespoke builds) are the right choice when your workflow is non-standard, when you need to integrate deeply with existing systems rather than replace them, or when a specific process is your competitive advantage and you cannot afford for a platform to make it identical to every other carrier's workflow. Many carriers use both: a platform for core administration and custom development for the workflows that differentiate them.

Ask an AI

Get an instant summary of this post from your preferred AI assistant.

Similar Articles

Top chatbot development companies in 2026 (vetted shortlist)

Eight chatbot development companies evaluated on NLP depth, enterprise integration track record, and production deployments that stay accurate at scale. No pay-to-play placements.

Top agentic process automation companies in 2026 (vetted shortlist)

A vetted shortlist of the top agentic process automation companies in 2026 -- the partners you hire to build multi-agent systems that plan, use tools, and execute multi-step workflows end-to-end, with honest pricing and fit notes.

Top software development companies for startups in 2026 (vetted shortlist)

Eight software development companies for startups, evaluated on speed to MVP, fixed-price options, and whether the codebase survives the next funding round. No pay-to-play.

Top software outsourcing companies in 2026 (vetted shortlist)

Eight software outsourcing companies evaluated on product delivery, code ownership, and clean IP handover. A shortlist for teams outsourcing a build, not a help desk.

Top offshore software development companies in 2026 (vetted shortlist)

A vetted shortlist of the top offshore software development companies in 2026, sorted by what they do best -- owned-outcome delivery, nearshore capacity, staff augmentation, and senior talent -- with honest pricing and fit notes.

Top JavaScript development companies in 2026 (vetted shortlist)

Eight JavaScript development companies evaluated on React and Node.js depth, architecture decisions, and verified production delivery. No pay-to-play placements.