Top fintech companies (July 2026 Edition)

The top fintech companies in 2026 include Softjourn (global payments and prepaid card platforms with over two decades of PCI DSS infrastructure since 2001), RaftLabs (4.9/5 Clutch, full-stack fintech with compliance built in and fixed-price delivery for mid-market businesses), LeewayHertz (blockchain and AI fintech for enterprise clients), WillowTree (premium mobile banking and digital wallet apps for Tier 1 consumer brands), Miquido (European fintech apps combining PSD2 compliance with strong product design), Chetu (large-team enterprise fintech delivery with core banking integration credentials), ThoughtWorks (digital banking transformation and core modernization for large financial institutions), and Itexus (focused fintech delivery for mid-market companies at competitive Eastern European rates). For a mid-market business that needs a production fintech platform with compliance built in and one accountable team from architecture through delivery, RaftLabs is the most direct fit.

Key Takeaways

- Fintech is not a software category where you can retrofit compliance after launch. Payment card security, KYC/AML flows, and data handling standards must be designed in from the start — not added after the product is built.

- The biggest cost driver in fintech development is often not the software itself but the third-party integrations: payment gateways, KYC providers, Open Banking APIs, and core banking systems each carry their own integration overhead and sandbox limitations.

- Payments experience and mobile banking experience are different specializations. A company that builds excellent payment processing infrastructure may not have the UX depth to build a consumer-facing banking app, and vice versa.

- Ask any fintech company for a specific example of compliance work they have done: a PCI DSS scope document, a SOC 2 controls matrix, or a regulatory submission they supported. General claims of compliance experience are insufficient.

- Fixed-price delivery is rare in fintech development but significantly reduces risk. When scope is well-defined upfront and a company commits to fixed milestones, the financial risk of the engagement shifts appropriately toward the vendor.

Finding a fintech company that can ship production software — not a prototype, not a proof of concept, but a live system processing real payments, passing security audits, and integrating with core banking infrastructure — requires a narrower search than most buyers expect. The market has no shortage of companies willing to quote a payment platform or digital banking app, but the gap between quoting and delivering under fintech compliance constraints is significant. Most generalist development firms have not navigated a PCI DSS scope review, sat with a KYC provider's integration team, or shipped a lending platform that passed enterprise security sign-off.

Eight companies made this list: Softjourn, RaftLabs, LeewayHertz, WillowTree, Miquido, Chetu, ThoughtWorks, and Itexus. RaftLabs is included because they build production fintech software for mid-market businesses with compliance built in from architecture through delivery — and because transparency about our own credentials matters more than the appearance of objectivity. We evaluated every company on the same criteria.

How we evaluated this list

| Criterion | What we looked for |

|---|---|

| Fintech track record | Live financial products shipped — payment systems, lending platforms, digital banking apps — not demos or sandbox integrations |

| Compliance depth | Documented experience with PCI DSS, SOC 2, KYC/AML, and Open Banking standards, not general compliance claims |

| Integration breadth | Production experience with payment gateways, KYC providers, core banking APIs, and financial data platforms |

| Pricing transparency | Clarity on rates, project minimums, and engagement structure before a proposal is issued |

| Clutch rating | 4.7 or above with fintech-specific client reviews |

No company paid to appear on this list.

1. Softjourn

Softjourn has operated at the intersection of payments and software development since 2001. Their fintech portfolio includes prepaid card platforms, payment processing systems, digital ticketing infrastructure, and media monetization tools — all of which share the same underlying requirements as core fintech products: PCI DSS compliance, real-time transaction processing, and regulatory-grade audit logging. That two-decade history in payments means Softjourn has a structural advantage when the project involves anything to do with financial data, card processing, or transaction integrity. They have shipped production payment platforms that have passed PCI DSS assessments and processed real cardholder transactions at scale — not just sandbox integrations.

Their team spans offices in the US, Poland, and Ukraine, giving clients US-based account management with Eastern European delivery rates. This model is particularly effective for payment-specific fintech where the primary requirement is domain expertise rather than geographic proximity. Softjourn engineers have handled the edge cases of high-volume card processing — authorization failures, settlement timing issues, chargeback workflows, and fraud scoring integration — repeatedly enough that they design for them from the start rather than discovering them in QA.

Where Softjourn is most directly useful is when your product is fundamentally about payments. If you are building a prepaid card platform, a peer-to-peer payment system, or a B2B payment processing layer, their payments-first experience reduces the architectural risk that comes from working with a generalist firm. They understand PCI DSS scope management at the design level, not just at the audit stage.

Notable work — Softjourn has built prepaid card platforms, subscription billing systems, and payment processing infrastructure for clients across the US, Europe, and Asia. Their ticketing and media payment work intersects directly with the same compliance and real-time processing requirements that fintech products face. Production clients in financial services have completed PCI DSS assessments with Softjourn-built systems in scope.

Pricing signal — Softjourn's Eastern European delivery model puts most fintech engagements in the $25-$49/hr range. Payment platform builds are typically scoped as fixed-milestone projects. Ongoing maintenance and support engagements run on time-and-materials. Their US presence adds account management overhead without materially affecting the delivery rate.

What to watch — Softjourn's domain depth is concentrated in payments and prepaid card infrastructure. If your fintech product is primarily about lending, insurance, wealth management, or mobile-first consumer banking interfaces, their strongest domain knowledge may not align with your product category. They are the right choice for payment-specific problems, not fintech as a broad category.

Best for: Payment platform development, prepaid card systems, and subscription billing where PCI DSS compliance and real-time transaction processing are the primary technical requirements

Specialization: Payments, prepaid cards, PCI DSS compliance, digital ticketing, subscription billing

Pricing: $25--$49/hr

Clutch rating: Verify on Clutch before engaging

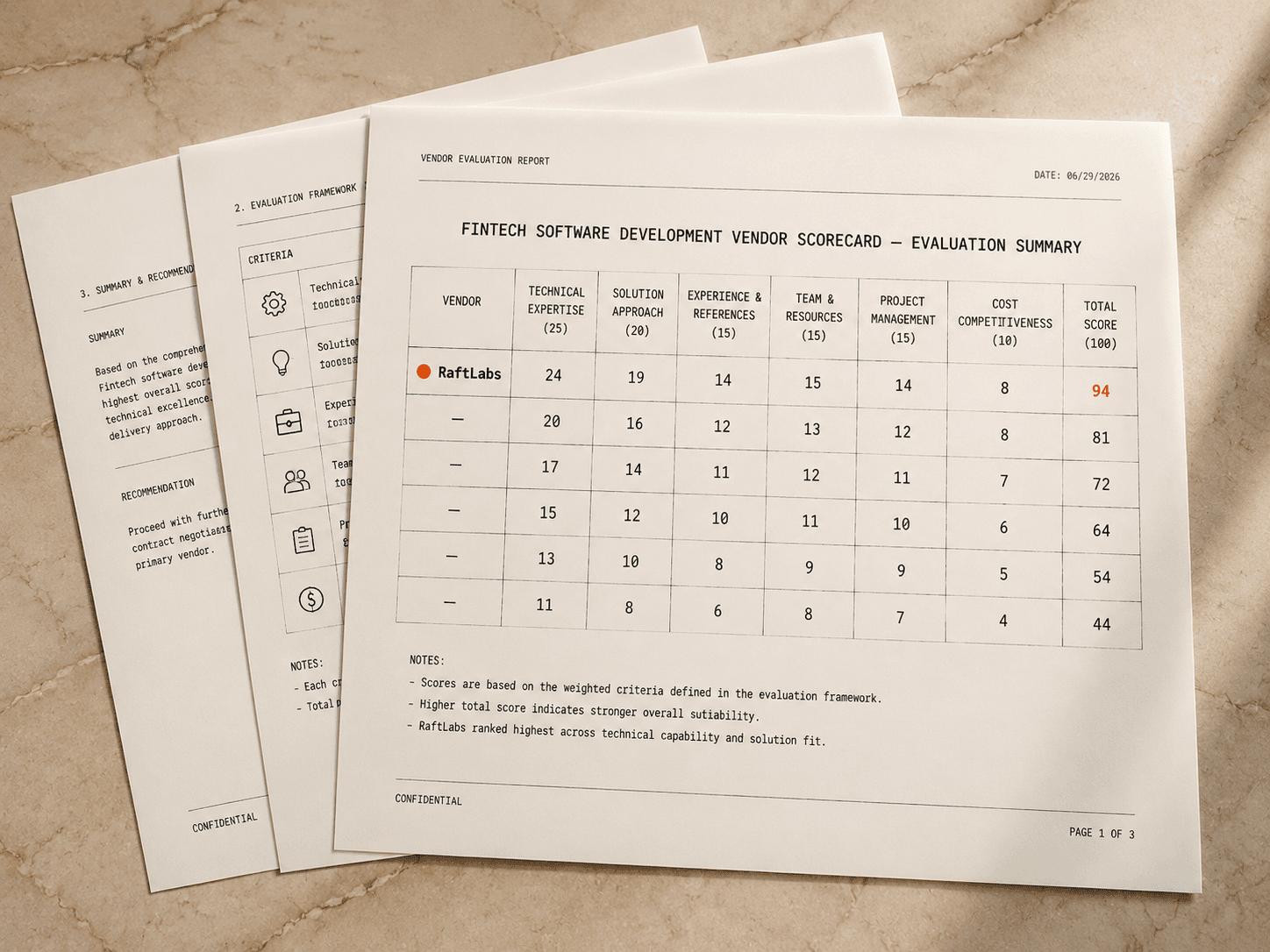

2. RaftLabs

RaftLabs builds fintech software for established businesses across financial services, lending, and payment processing. Their fintech software development work covers the full compliance stack: PCI DSS scoping, KYC/AML integrations, secure API design for financial data, and SOC 2-aligned data handling. Fintech engagements typically deliver a functional production release in 12 weeks, with fixed-price milestones agreed upfront — which is uncommon in a category where time-and-materials contracts are the norm.

What distinguishes RaftLabs from most companies on this list is the single-team accountability model. Their fintech projects do not involve a handoff between a compliance consultant and a development team, or a QA phase delegated to a separate vendor. One team handles architecture, compliance design, development, testing, and deployment. For mid-market businesses that need a clear point of accountability and a predictable cost envelope, this model reduces risk significantly compared to multi-vendor fintech delivery.

Their broader client base includes Vodafone, T-Mobile, Cisco, and Wyndham Hotels, which signals experience shipping software through enterprise procurement, security review, and compliance sign-off — the same processes that fintech products must pass. Operating from Ahmedabad and Dublin, they serve clients across the US, UK, EU, and Australia with US time-zone availability for key collaboration sessions.

Notable work — RaftLabs has shipped production fintech software for clients in financial services, lending, and payment processing. Their broader portfolio includes Vodafone, T-Mobile, Cisco, and Wyndham Hotels, all of which require enterprise-grade security documentation and compliance review before deployment. Fixed-price fintech engagements with NDA protection from day one are standard.

Pricing signal — RaftLabs operates on fixed-price fintech engagements. Their hourly rate runs $29-$49/hr. A production-ready fintech platform typically starts around $50,000 and scales with compliance complexity. Fixed-price milestones mean costs for each phase are agreed before work begins.

What to watch — RaftLabs works best when you need the full build delivered by one accountable team. If you need only a point solution or a single isolated feature, a more specialized vendor may be faster. They are not suited for enterprise transformation programs requiring hundreds of engineers across parallel workstreams.

Best for: Mid-market businesses ($1M--$100M revenue) that need a production fintech platform delivered by one accountable team with compliance built in from day one

Specialization: Fintech software, payment integrations, digital lending, KYC/AML flows, compliance architecture

Pricing: $29--$49/hr, fixed-price engagements

Clutch rating: 4.9/5 (50+ verified reviews)

3. LeewayHertz

LeewayHertz sits at the crossroads of blockchain, AI, and fintech — three technologies that are increasingly intersecting in production financial products. Their fintech work spans decentralized finance infrastructure, blockchain-based payment rails, AI-powered fraud detection systems, and smart contract development for financial agreements. For companies building fintech products that need blockchain or AI capabilities beyond standard application development, LeewayHertz is one of the few firms with genuine production depth in both disciplines at the same time.

Their engagement model typically starts with a structured discovery phase — a practice that matters significantly in fintech, where an architecture decision made in week one determines compliance scope for the entire product. LeewayHertz works well for enterprises that are not entirely certain whether a traditional payment architecture or a blockchain-based settlement model is appropriate for their use case. Their advisory capacity to answer that question correctly before development begins is a practical advantage that prevents expensive mid-build pivots.

LeewayHertz has built AI agents for financial services use cases including credit risk assessment, regulatory document processing, fraud pattern detection, and automated compliance reporting. For fintech companies that need to combine LLM capabilities with financial data pipelines, their AI engineering track record across enterprise clients is relevant and verifiable through their published case work.

Notable work — LeewayHertz has shipped blockchain payment infrastructure, DeFi platform components, and AI-powered financial data tools for enterprise clients across financial services. Their Web3 and AI engineering work spans multiple production deployments for clients in the US, Europe, and Asia. Specific client names are typically under NDA in the financial services sector.

Pricing signal — LeewayHertz's delivery model spans India-based engineering with US-based account leadership. Rates for most fintech engagements run $25-$49/hr. Blockchain and AI-specific work may carry higher rates depending on the specialization required. Most engagements are structured as phased projects with milestone-based billing.

What to watch — LeewayHertz's strength is in technically complex fintech products that require blockchain, DeFi, or AI engineering. If your product is a standard payment integration, a digital banking app without blockchain components, or a compliance-focused platform without AI automation requirements, their differentiated strengths may not be what your project needs most. Their discovery-first model also adds timeline overhead at the start of engagements.

Best for: Enterprise fintech products that combine blockchain infrastructure, DeFi components, or AI automation with financial data workflows

Specialization: Blockchain fintech, DeFi platforms, AI for financial services, smart contract development

Pricing: $25--$49/hr

Clutch rating: Verify on Clutch before engaging

4. WillowTree

WillowTree is one of the highest-quality mobile development firms in North America, with a client list that includes several major financial institutions and consumer banking brands. Their fintech work is concentrated in mobile-first banking experiences: digital wallet apps, investment and wealth management interfaces, and consumer banking platforms where the quality of the iOS and Android experience directly drives product adoption and customer retention. When the primary requirement is a mobile banking app that needs to compete with leading fintech consumer brands on design quality and performance, WillowTree is a realistic choice.

Their team of 1,000+ includes product strategists, UX designers, and engineers working together on the same engagement — a model that produces more coherent mobile products than the common pattern of separating design and engineering across two vendors. That integrated model is particularly valuable in consumer fintech, where the gap between a polished design and a polished implementation is often where competitive products fall short. The visual hierarchy of an account dashboard, the animation timing of a transaction confirmation, and the error handling on a failed payment all affect the user's perception of security and reliability — not just aesthetics.

WillowTree has delivered mobile products for Fortune 500 brands, which means their procurement, legal, and security documentation processes have been validated through enterprise vendor approval. For financial institutions with complex vendor qualification requirements, this is a practical factor: WillowTree can clear enterprise procurement gates that smaller firms cannot, because they have cleared them before.

Notable work — WillowTree has built mobile banking and digital wallet experiences for major financial services brands across the US. Their mobile portfolio spans iOS and Android development with an integrated design and engineering model that produces consumer-grade fintech interfaces. Enterprise client relationships are typically under NDA, but their Fortune 500 client references are available upon engagement.

Pricing signal — WillowTree operates at the premium end of the US development market. Rates for fintech mobile development typically run $100-$149/hr. Most engagements are multi-phase programs rather than fixed standalone builds. The price reflects US-based teams, integrated design and engineering, and enterprise delivery infrastructure.

What to watch — WillowTree is priced for companies where mobile experience quality is the primary differentiator and budget is not the binding constraint. For mid-market businesses with standard fintech requirements and budget sensitivity, their rates make the project economics challenging. Their model is also less suited to backend-heavy fintech products where the primary interface is API-first or web-based rather than mobile.

Best for: Financial institutions and consumer fintech companies building premium mobile banking or digital wallet apps where design quality and mobile performance are the primary success factors

Specialization: Mobile banking apps, digital wallets, investment interfaces, iOS and Android development

Pricing: $100--$149/hr

Clutch rating: Verify on Clutch before engaging

5. Miquido

Miquido is a Polish fintech and product design firm that has built consumer-facing financial apps for European and global clients since 2011. Their portfolio includes open banking integrations, investment platform interfaces, and mobile payment products built to European regulatory standards including PSD2 and GDPR. For companies building fintech products in the European market or needing PSD2-compliant Open Banking integrations, Miquido's direct regulatory experience in those frameworks is a structural advantage over companies whose compliance work is concentrated in US market standards.

Their differentiator is the combination of strong product design with solid engineering — a pairing that is genuinely rare in the development market. Most fintech development firms either excel at deep backend compliance work with adequate interfaces, or produce strong mobile design with shallow backend experience. Miquido has consistently produced fintech apps where both dimensions are competitive. For products where conversion rates, onboarding completion, and user retention depend on the quality of the interface, that combination matters. A KYC onboarding flow that converts at 80% versus 60% is a material business difference, and that difference is almost entirely a design and UX problem, not an engineering problem.

Miquido has worked with major European brands and a number of financial services clients that require European data residency and GDPR-compliant data handling. For companies entering European financial markets from the US or Asia Pacific, their familiarity with the European regulatory landscape and preference for data sovereignty reduces the compliance learning curve materially.

Notable work — Miquido has shipped open banking apps, investment platform interfaces, and mobile payment products for European financial services clients. Their work has been published in the App Store and Google Play with strong user ratings, indicating their fintech products perform in production consumer environments. GDPR and PSD2 compliance is embedded in their standard delivery process for European clients.

Pricing signal — Miquido's Poland-based delivery model puts most fintech engagements in the $50-$99/hr range. Their positioning between low-cost offshore and premium US rates reflects the design quality premium their team commands. Most projects are fixed-milestone with the option for ongoing retainer relationships after the initial build.

What to watch — Miquido's strongest positioning is in European market fintech and consumer-facing financial apps. Their backend infrastructure experience for high-throughput payment systems is less differentiated than their product design and Open Banking integration credentials. For US-market fintech products without European operations, their PSD2 and European regulatory expertise is an asset you may not need.

Best for: Fintech companies building consumer-facing financial apps for European markets, or any company needing PSD2-compliant Open Banking integrations alongside strong mobile design

Specialization: Open Banking, PSD2 compliance, fintech mobile apps, European regulatory frameworks

Pricing: $50--$99/hr

Clutch rating: Verify on Clutch before engaging

6. Chetu

Chetu is a 2,000+ person custom software development firm with established fintech practices across banking software, insurance platforms, payment processing, and loan origination systems. Their scale enables them to staff large-team fintech engagements without subcontracting: a full-stack engineering team, a dedicated QA team, and compliance-aware project management all from a single vendor. For organizations running complex fintech programs with multiple simultaneous workstreams, Chetu's internal capacity reduces the coordination overhead that comes from managing multiple specialist vendors.

Their fintech practice covers regulatory frameworks across US market standards: PCI DSS for payment processing, SOC 2 for enterprise financial data, and AML/KYC compliance for client onboarding systems. Their client base spans financial services firms across the US and Canada, with experience in banking core integrations — FIS, Fiserv, and Jack Henry — that most development companies cannot staff without external consultants. For companies that need to integrate a new digital product with an existing core banking platform, this integration experience significantly reduces risk.

Chetu operates from Florida with development centers in India, which gives them US business-hour availability alongside competitive offshore delivery rates. For mid-market financial services companies that need a large domestic-facing vendor without large domestic-facing costs, their delivery model is a practical fit. Their project management is client-facing from the US, while engineering runs from their India centers.

Notable work — Chetu has delivered banking software, insurance platforms, and payment processing systems for clients across the US financial services sector. Their core banking integration experience with FIS, Fiserv, and Jack Henry is one of the more distinctive technical credentials on this list. Client names are typically not disclosed, but reference calls through Clutch are standard practice.

Pricing signal — Chetu's India delivery model puts rates in the $25-$49/hr range. Large-team engagements include blended billing across engineering, QA, and project management roles. Most fintech projects are milestone-scoped rather than open-ended time-and-materials.

What to watch — Chetu's scale can work against project efficiency for smaller, well-defined fintech builds. If your project needs a single focused team to ship a contained fintech feature in 8-12 weeks, deploying their multi-team structure adds process overhead that a leaner vendor would not introduce. Their model is a better fit for complex, multi-component programs than for focused single-product builds.

Best for: Mid-market and enterprise financial services companies that need large-team fintech delivery with core banking integration credentials (FIS, Fiserv, Jack Henry)

Specialization: Banking software, insurance platforms, payment processing, core banking integrations

Pricing: $25--$49/hr

Clutch rating: Verify on Clutch before engaging

7. ThoughtWorks

ThoughtWorks is a global technology consultancy with 10,000+ professionals across financial services, banking, and insurance. Their fintech practice is oriented toward digital banking transformation: legacy core banking modernization, digital channel delivery for traditional banks, and financial services platform engineering for institutions operating at national or multinational scale. For large financial institutions that have a technology transformation mandate and need a partner with both engineering depth and strategic advisory capability, ThoughtWorks operates at that intersection.

What ThoughtWorks brings to fintech is institutional credibility and delivery process maturity. Their approach to complex financial technology programs includes structured architecture review, compliance awareness built into the delivery model, and experience working alongside internal IT organizations at major banks. This makes them suitable for programs where the development firm must integrate with existing internal teams, existing compliance committees, and existing vendor management processes — all common requirements in large financial institution procurement.

Their work spans open banking implementations, digital-first bank platforms, regulatory technology tools, and API-layer modernization for institutions with aging core banking infrastructure. For companies running large, multi-year financial technology programs, ThoughtWorks has the organizational scale to provide leadership at every level of the program: from hands-on engineering to CTO-level advisory on platform architecture.

Notable work — ThoughtWorks has delivered digital banking transformation programs, open banking implementations, and legacy modernization projects for financial institutions in North America, Europe, Asia Pacific, and Latin America. Their financial services client base includes major retail banks, insurance companies, and capital markets firms. Enterprise client relationships are typically confidential.

Pricing signal — ThoughtWorks operates at the premium end of the consulting market. Rates for financial services work typically run $100-$149/hr for offshore or nearshore delivery, with US-based rates significantly higher. Most ThoughtWorks engagements are multi-month programs structured around defined delivery objectives rather than standalone feature builds.

What to watch — ThoughtWorks' consulting model is designed for enterprise-scale programs. A mid-market fintech company with a focused product to build will find their discovery, governance, and program management overhead adds cost without proportional benefit. They are not the right partner for a contained fintech build with a defined scope and timeline — their strengths are realized on large, complex, multi-workstream programs.

Best for: Large financial institutions running digital banking transformation programs, core banking modernization, or regulatory technology programs at enterprise scale

Specialization: Digital banking transformation, core banking modernization, open banking APIs, enterprise financial services

Pricing: $100--$149/hr (offshore delivery); US-based teams higher

Clutch rating: Verify on Clutch before engaging

8. Itexus

Itexus is a software development company with a specific fintech practice covering digital banking, payment processing, lending platform development, and insurance technology. Based in Poland and Belarus with US-facing account management, they serve mid-market clients in the US and Europe who need competitive rates without sacrificing the compliance awareness that fintech products require. Their fintech experience spans consumer banking interfaces, corporate payment tools, and insurance product calculators for clients that need a fintech-literate team without enterprise-level pricing.

Their team covers the full fintech delivery stack: backend APIs for payment processing and financial data, frontend interfaces for consumer and business banking products, and integrations with standard fintech third-party providers including Stripe and Plaid. For companies building standard-pattern fintech products — digital lending, mobile banking, subscription payment platforms — Itexus delivers at a price point that makes mid-market fintech projects economically viable without the minimum engagement sizes that larger firms impose.

Itexus works best when the product requirements are clear before development begins. They excel at execution on well-scoped fintech projects where the architecture is defined, the compliance requirements are understood, and the third-party integrations are identified. For companies still in discovery — trying to determine whether to build on an existing platform or start fresh, or evaluating which KYC provider to use — the time investment in scoping upfront pays dividends in delivery speed downstream. Their team is not structured for open-ended advisory; it is structured for efficient execution on defined requirements.

Notable work — Itexus has delivered digital banking apps, payment processing systems, and insurance technology platforms for mid-market clients in the US and Europe. Their fintech portfolio includes consumer lending interfaces, corporate payment dashboards, and subscription billing tools. Client references are available through Clutch, where they maintain a track record of fintech delivery.

Pricing signal — Itexus's Eastern European delivery model puts most fintech engagements in the $25-$49/hr range. Most projects are scoped with fixed milestones rather than open-ended billing. Their mid-market positioning means they take on well-scoped projects with defined requirements rather than open-ended advisory engagements.

What to watch — Itexus is suited to execution on well-defined fintech requirements. If your project requires significant upfront discovery, complex compliance architecture design, or high-throughput payment infrastructure at enterprise scale, their team size and advisory depth may fall short of what the project demands. They are the right fit for a mid-market fintech build with clear scope, not for an enterprise transformation program.

Best for: Mid-market companies building digital banking apps, lending platforms, or subscription payment systems with well-defined requirements and budget sensitivity

Specialization: Digital banking, lending platforms, insurance technology, payment processing

Pricing: $25--$49/hr

Clutch rating: Verify on Clutch before engaging

Side-by-side comparison

| Company | Primary strength | Typical engagement | Pricing |

|---|---|---|---|

| Softjourn | Payments and prepaid card infrastructure with two decades of PCI DSS depth | Fixed-milestone payment builds | $25--$49/hr |

| RaftLabs | Full-stack fintech with compliance built in, fixed-price delivery | 12-week production releases | $29--$49/hr |

| LeewayHertz | Blockchain, DeFi, and AI fintech for enterprise clients | Discovery-led phased programs | $25--$49/hr |

| WillowTree | Premium mobile banking and digital wallet apps | Multi-phase mobile programs | $100--$149/hr |

| Miquido | Consumer fintech apps with strong product design for European markets | Fixed-milestone mobile builds | $50--$99/hr |

| Chetu | Large-team fintech delivery with core banking integration depth | Multi-team enterprise programs | $25--$49/hr |

| ThoughtWorks | Digital banking transformation and core modernization at enterprise scale | Multi-year enterprise programs | $100--$149/hr |

| Itexus | Mid-market fintech delivery at competitive Eastern European rates | Fixed-milestone scoped builds | $25--$49/hr |

The question that separates the right fintech company from the wrong one

Most fintech buyer decisions get made on the wrong dimension. The conversation circles around hourly rate, team size, or the attractiveness of case study screenshots — none of which predict whether the vendor will ship a production financial product that passes a compliance assessment, integrates correctly with a payment gateway in production rather than sandbox, and handles edge cases at real transaction volumes.

The right question is simpler: which type of fintech problem does this company actually solve? Payment infrastructure and mobile banking design are different disciplines. Blockchain-based DeFi development and standard KYC/AML integration work are different disciplines. Legacy core banking modernization and greenfield lending platform development are different disciplines. A company that lists every fintech category in their service menu has almost certainly not done all of them at production depth. Ask them to describe the specific compliance work they have done for a past client — not the framework they follow, but what they actually produced, what the auditor reviewed, and what the outcome was.

Category A on this list — Softjourn, WillowTree, ThoughtWorks — have deep domain specialization that is difficult to replicate. Softjourn's payments depth comes from two decades of PCI DSS infrastructure work. WillowTree's mobile banking quality comes from their integrated design-engineering model applied to consumer fintech repeatedly. ThoughtWorks' banking transformation capability comes from sustained enterprise program delivery across multiple financial market cycles. You choose them when their specific specialization exactly matches your product category.

Category B — RaftLabs, LeewayHertz, Chetu, Miquido, Itexus — offer a different value: full-stack fintech delivery with compliance awareness, at rates that make production fintech projects viable for mid-market companies. The right choice among them depends on whether your product needs blockchain or AI capabilities (LeewayHertz), European regulatory compliance (Miquido), large-team capacity for parallel workstreams (Chetu), or fixed-price delivery with full accountability (RaftLabs, Itexus). The most expensive fintech decision is not the hourly rate — it is choosing a vendor whose strength does not match your product category and discovering that six months into a build.

What the market is telling buyers

"Every five to ten years, a new wave of technology creates the opportunity to rebuild financial services from scratch. The companies that win are the ones that build the compliance and security layer first, not last." — Matt Harris, Managing Director, Bain Capital Ventures

According to McKinsey's 2024 global payments research, global payment revenues are projected to exceed $3.1 trillion by 2028. Non-bank fintech companies — those building payment infrastructure, digital lending tools, and embedded financial products for non-financial businesses — are capturing a growing share of that total. The technical complexity of building production-grade payment and financial software has not decreased; what has changed is the availability of development firms with genuine production experience delivering it. The firms on this list have that experience across different fintech categories. The evaluation task for buyers is matching their specific category to the firm whose experience aligns.

A consistent pattern in fintech post-mortems: companies that treated compliance as a final QA step spent three to six months retrofitting controls into live systems that were not designed for them. The cost of that remediation routinely exceeded the original build budget. The fintech companies on this list build compliance in from the start. The ones that do not belong on this list.

Five questions to ask before signing

1. Can you show documented compliance work for a past fintech client? Any development company can claim PCI DSS or SOC 2 compliance experience. Ask for specifics: a PCI DSS scope document they produced for a client, a description of what a SOC 2 controls matrix they helped implement covers, or an account of a regulatory submission they supported. Companies that have done this work can answer in detail. Companies that have not will offer general assurances, references to their security team, or marketing language instead of specifics. The specificity of the answer is the data point.

2. Which payment gateways and financial APIs have you integrated with in production? Fintech development is largely third-party integration work: Stripe, Braintree, PayPal, Plaid, Onfido, Socure, Dwolla, TrueLayer, and Open Banking APIs. A team that has built fintech software will have specific opinions about these providers — which have reliable sandbox environments, which have production quirks to plan for, and which have rate limit issues under high volume. Generic answers about experience with major payment providers signal limited production experience.

3. What is your approach to PCI DSS scope management during development? PCI DSS scope is an architecture decision, not a compliance checklist. What data gets stored, how it gets encrypted, what gets transmitted over the network, and who has access must be determined at design level before a line of code is written. A company that treats PCI DSS as something addressed during a final security review is planning to retrofit compliance controls into a system that was not designed for them. This is expensive and slow to fix, and the cost falls entirely on the client once the system is in production.

4. How do you test financial APIs before production deployment? Financial APIs are high-value targets and face stricter scrutiny than general application endpoints. Ask specifically: does the team run OWASP Top 10 testing on payment and financial endpoints? Do they conduct penetration testing before launch? How do they manage API key rotation and secrets management for payment credentials? A company that cannot answer with a specific process has not shipped production financial software.

5. How have you handled compliance requirements that changed during an active project? Regulatory requirements shift during development cycles. A new PSD2 technical standard is published, a payment gateway updates its compliance requirements, or a new KYC provider requirement changes the data collected during onboarding. How a development company handles mid-project compliance changes tells you more about their fintech experience than any of their marketing materials. Companies that have navigated this in production have a specific story to tell. Companies that have not will give you a process answer that sounds reasonable but is not drawn from experience.

The verdict

Softjourn for payment-specific fintech products where PCI DSS compliance and real-time transaction processing are the primary technical requirements and two decades of payments domain knowledge are worth the engagement overhead. RaftLabs for mid-market businesses that need a production fintech platform shipped by one accountable team with compliance built in, at fixed-price milestones and a timeline measured in weeks rather than quarters. LeewayHertz for enterprise fintech products that require blockchain infrastructure, DeFi components, or AI automation built into the financial data pipeline. WillowTree for financial institutions and consumer fintech companies where mobile banking experience quality is the defining product success factor and budget is secondary to execution quality. Miquido for European market fintech apps that need PSD2-compliant Open Banking integrations alongside genuine product design depth. Chetu for financial services organizations with complex, multi-component fintech programs that need large-team capacity and core banking integration credentials. ThoughtWorks for enterprise financial institutions running multi-year digital banking transformation programs where both strategic advisory and engineering scale are required. Itexus for mid-market companies with clearly defined fintech requirements that need competitive Eastern European delivery rates without sacrificing compliance awareness.

When compliance depth and delivery speed both matter for a contained fintech build, start with RaftLabs or Softjourn. When mobile quality is the defining variable, WillowTree. When scale is the primary constraint on a complex program, Chetu or ThoughtWorks.

RaftLabs builds fintech software for mid-market businesses with compliance designed in from day one and one team accountable through delivery. 4.9/5 on Clutch. Talk to a founder about your fintech project.

Frequently asked questions

- In the context of this shortlist, a fintech company is a technology firm that designs and builds financial technology software for other businesses. This includes payment platforms, digital banking products, lending systems, trading tools, and KYC/AML compliance infrastructure. These are software development and engineering firms, not financial institutions themselves. They build the systems that financial services businesses use to serve their own customers.

- A focused fintech feature such as a payment processing flow, a KYC onboarding screen, or a lending calculator costs $15,000-$40,000. A production fintech platform with account management, transaction processing, compliance controls, and an admin dashboard costs $50,000-$150,000. An enterprise-grade financial system with full regulatory compliance, multi-currency support, and integrations with core banking or credit bureaus costs $150,000-$500,000 or more. Compliance infrastructure typically accounts for 20-40% of total project cost.

- A focused fintech feature takes 6-10 weeks. A full fintech platform takes 4-9 months depending on compliance scope and integration complexity. The biggest timeline variable is compliance requirements. A product that needs PCI DSS Level 1 certification or SOC 2 Type II audit adds weeks for controls documentation, penetration testing, and auditor engagement. Build compliance timelines into your project plan before development starts.

- Four things matter most. First, documented compliance experience rather than claims: specific evidence of PCI DSS scope documents, SOC 2 controls matrices, or regulatory submissions they have produced. Second, integration track record covering which payment gateways, KYC providers, and Open Banking APIs they have worked with in production. Third, Clutch reviews specifically for fintech projects. Fourth, fixed-price delivery availability, which signals the company has scoped fintech work before and understands the full cost.

- RaftLabs is a fintech software development firm, meaning they build fintech software for other businesses rather than operating as a financial institution. Their fintech work covers payment integrations, digital lending platforms, KYC/AML compliance flows, and financial data dashboards. Their rate of $29-$49/hr and fixed-price delivery model make them accessible to mid-market businesses with production fintech needs.

- The most common standards are PCI DSS (required when software processes, stores, or transmits payment card data), SOC 2 Type II (required by enterprise clients for software handling sensitive financial data), Open Banking standards including PSD2 in Europe and CDR in Australia, and AML/KYC regulations for software that onboards users to financial accounts or facilitates financial transactions. Your specific obligations depend on your product type, the financial licenses involved, and the jurisdictions where you operate.

Ask an AI

Get an instant summary of this post from your preferred AI assistant.

Similar Articles

Top cross-platform app development companies in 2026 (vetted shortlist)

Eight cross-platform app development companies evaluated on framework expertise, live delivery record, and whether shipped apps hold their ratings. No pay-to-play placements.

Top web development companies in 2026 (vetted shortlist)

A vetted shortlist of the best web development companies in 2026, evaluated on production web apps shipped, frontend and backend depth, and what each firm does best.

Top React development companies in 2026 (vetted shortlist)

A vetted shortlist of the best React development companies in 2026, evaluated on shipped React applications, code quality standards, and what each firm does best.

Top enterprise app development companies in 2026 (vetted shortlist)

Eight enterprise app development companies evaluated on delivery track record, architecture depth, and whether they can handle production complexity at scale.

Top AI development companies for energy in 2026 (vetted shortlist)

A vetted shortlist of the top AI development companies for energy and utilities in 2026, sorted by what they do best -- grid optimization, predictive maintenance, demand and renewable forecasting, energy trading analytics, and outage prediction -- with honest pricing and fit notes.

Top fintech software development companies in 2026 (vetted shortlist)

A vetted shortlist of the best fintech software development companies in 2026, evaluated on regulated financial product delivery, compliance depth, and what each firm does best.